(Image Credit: Supplied)

Sponsored

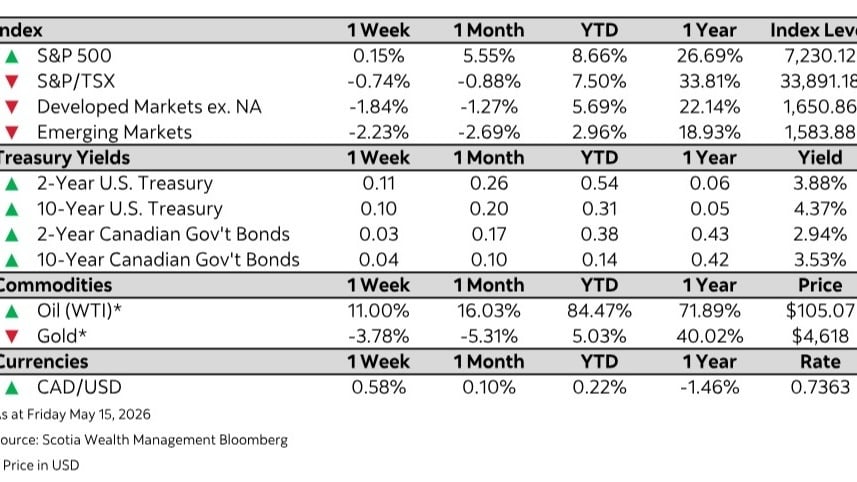

Market Watch — May 15, 2026

May 19, 2026 | 11:47 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Tech strength supported U.S. markets as oil prices pressure cyclicals

- Global rates move higher on persistent geopolitical risks, rising inflation

- Canada’s wholesale sales climb in March, driven by machinery and equipment gains

- U.S. inflation rises to 3.8% in April, driven by energy prices

- Eurozone growth stalls as latest GDP data shows fragile recovery