Sponsored

Market Watch: February 16

Feb 20, 2024 | 5:24 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

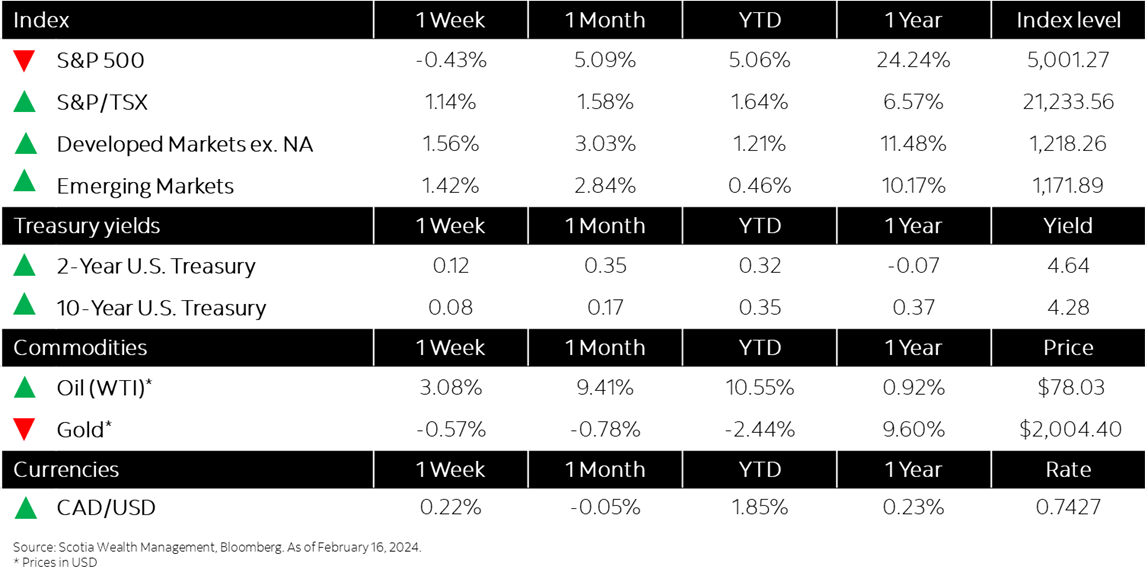

- U.S., international markets diverge on a recalibration of expectations

- Bond yields move higher following inflation readings

- Canadian building permits dropped 14% in December from November

- U.S. consumer prices rose more than expected in January

- Eurozone industrial production unexpectedly expands amid signs of recovery for sector

- In the news: Airbus extends lead over Boeing amid fallout over safety incidents

Week in review

U.S., international markets diverge on a recalibration of expectations