Sponsored

Market Watch: July 21

Jul 21, 2023 | 4:10 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

WEEK IN REVIEW

GLOBAL MARKETS GIVE UP SOME GAINS LATE IN THE WEEK

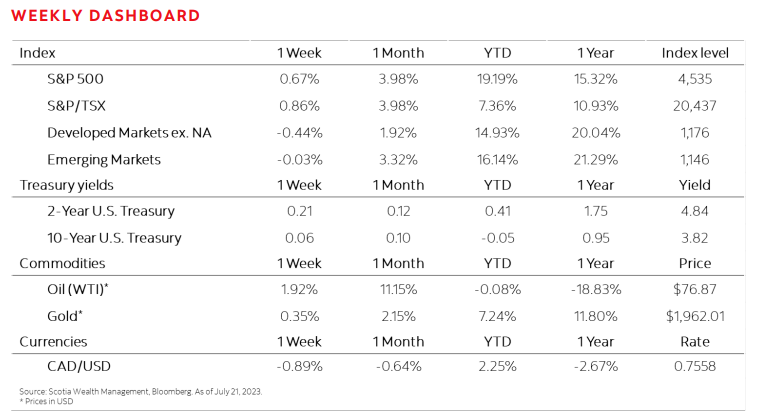

U.S. equities managed to stay in the black, returning 0.67%1 , after posting relatively strong gains for the first half of the week but giving a large portion of it up following post-earnings declines from Netflix and Tesla. Canadian markets traded within a narrow band, managing to return 0.86%2, held up by rate-sensitive sectors. European markets were -0.44%3 lower for the week with gains in the health care sector being offset by declines in chip stocks. Emerging markets were also -0.03%4 lower amid an ongoing slump in Chinese economic growth, with pledges for further support from policymakers failing to assuage investors’ concerns.

Highlights: