sponsored

Market Watch: August 4, 2023

Aug 5, 2023 | 11:53 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

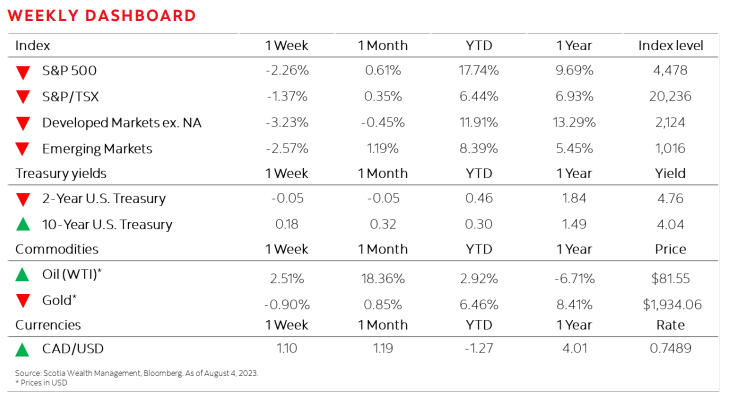

WEEK IN REVIEW

MARKETS REVERSE COURSE FRIDAY FOLLOWING STRONG JOBS REPORT

After a period of choppy trading that saw mega-cap tech stocks trade lower mid-week, a strong U.S. jobs report put a bid back under equity markets but was not enough to reverse previous losses. Investors assessed the latest batch of earnings and the cooler-than-expected July jobs report. Bullish sentiment seems to have returned after this latest report with nearly 87% of traders now expecting the U.S Federal Reserve (Fed) to hold rates steady at its next meeting in September.

Highlights: