(Image Credit: Scotia Wealth Management)

Sponsored

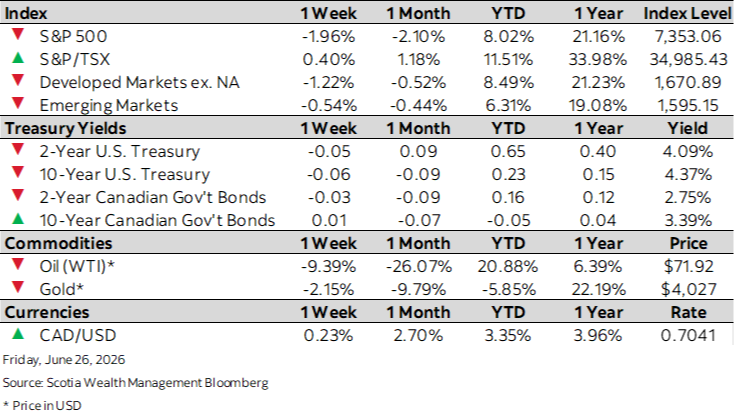

Markey Watch – June 26, 2026

Jun 29, 2026 | 9:53 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

A summary of the week’s important events and how they could impact the market.

This week’s highlights

- AI volatility drives a choppy week for global equities

- Bonds rally as oil retreats and PCE cools rate hike concerns

- Canadian headline inflation rises, but core measures remain contained

- Rate hike bets cool as U.S. inflation signals remain mixed

- Eurozone business activity stabilizes, though still in contraction, PMI shows