Sponsored

Market Watch — May 29, 2026

May 29, 2026 | 4:45 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

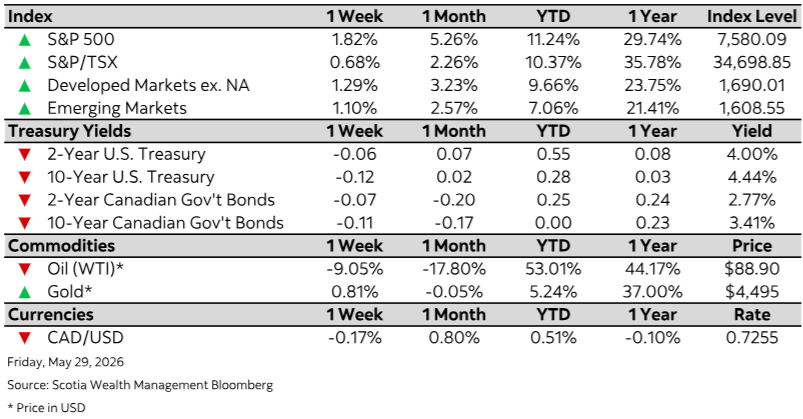

This week’s highlights

- Strong earnings season drives returns as markets await geopolitical clarity

- Optimistic geopolitical headlines drive modest decline in yields

- Canada’s economy unexpectedly contracted for a second straight quarter

- U.S. data highlights softer growth alongside persistent inflation pressures

- French economy contracts, Italy sees modest growth in 1Q