(Image Credit: Scotia Wealth Management)

Sponsored

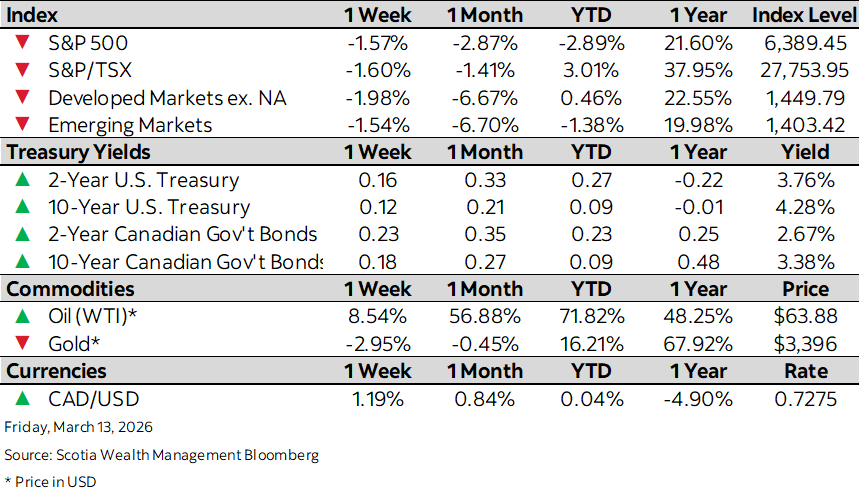

Market Watch: March 13

Mar 13, 2026 | 4:10 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Positive corporate and economic news overshadowed by Middle East conflict

- Global yields continue to climb on energy-linked inflation concerns

- Canada’s trade deficit widens to $3.65 billion in January on auto weakness

- U.S. inflation held steady in February before Iran war sent energy costs soaring

- Eurozone fourth-quarter growth revised lower