(Image Credit: Scotia Wealth Management)

Sponsored

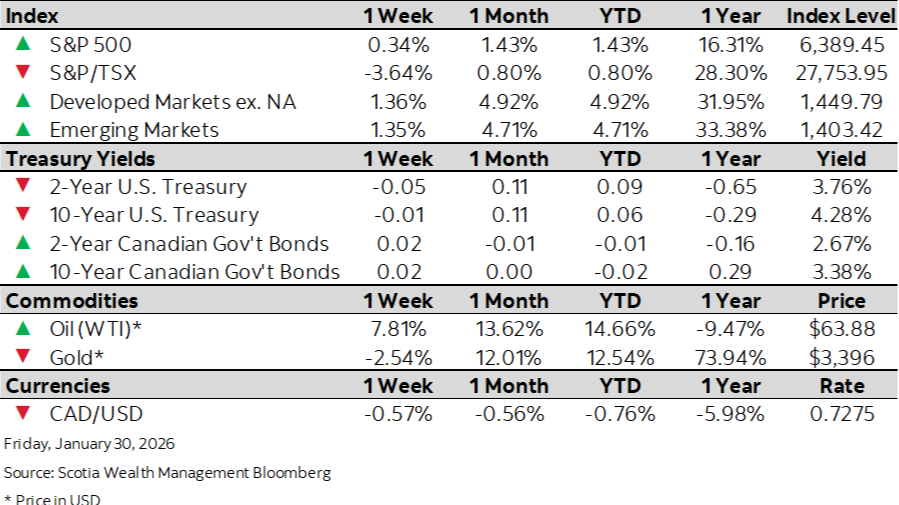

Market Watch: February 6

Feb 9, 2026 | 1:02 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

A summary of the week’s important events and how they could impact the market.

This week’s highlights

- Precious metals and tech pullback clash with hawkish Fed chair nomination

- Sovereign curves move on soft hiring signals and central bank caution

- Canada services PMI moves lower as activity and new business decline

- U.S. private payrolls undershoot expectations in January

- Eurozone inflation sinks below ECB target