sponsored

Market Watch – Aug. 2, 2025

Aug 5, 2025 | 11:41 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

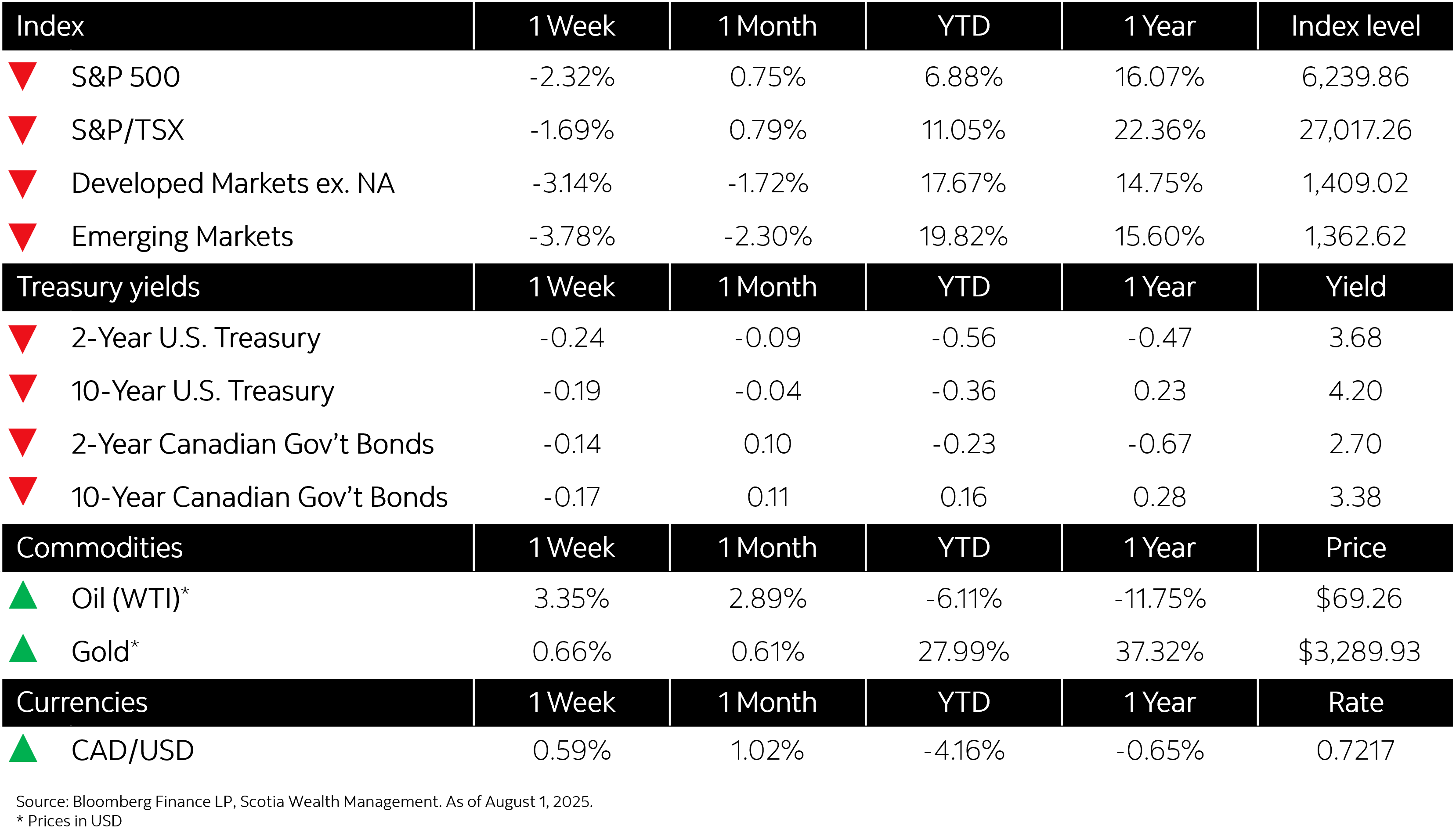

This week’s highlights

- Barrage of central bank decisions, economic data and tariffs push markets lower

- Short-term U.S. Treasury yields decline as market anticipates rate cut in the fall

- Bank of Canada holds key rate, says economy weathered tariffs better than expected

- U.S. economy rallies in second quarter, with higher-than-expected GDP growth of 3%

- Eurozone economy shows signs of resilience even as tariffs bite