sponsored

Market Watch: April 4, 2025

Apr 7, 2025 | 10:19 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

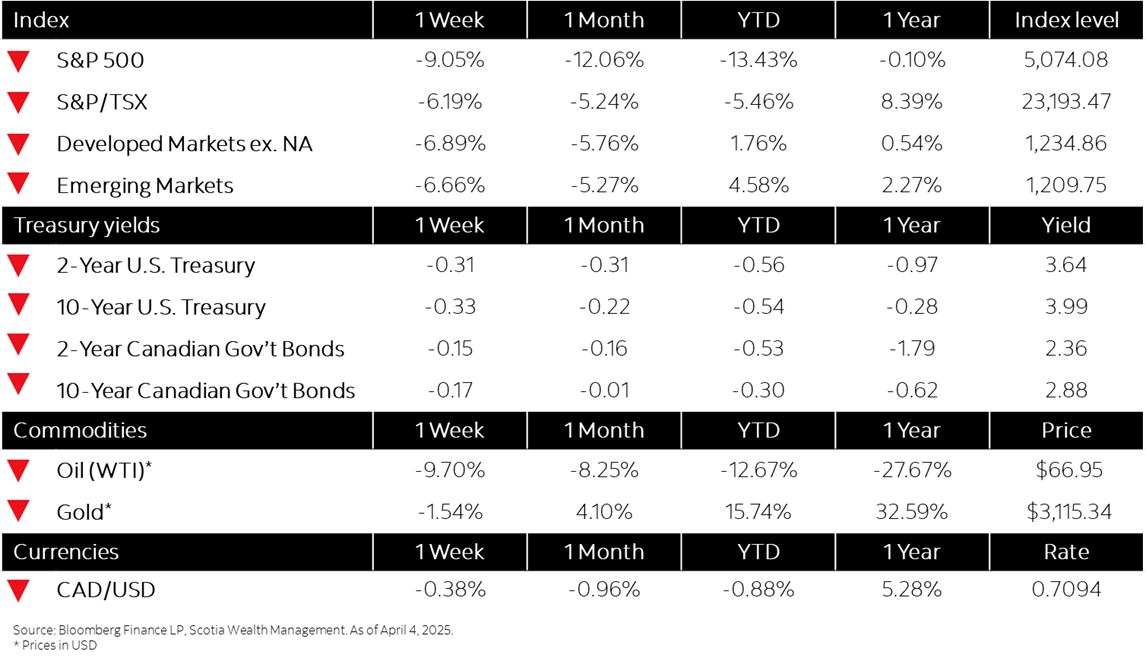

This week’s highlights

- Equity markets on the backfoot as tariffs shake up global trade

- Sovereign yields move lower, credit spreads widen amid broad risk-off sentiment

- Canadian factory PMI hits 15-month low on widening global trade war

- U.S. hiring defied expectations in March, with 228,000 new jobs

- Eurozone inflation falls close to target, but price pressures remain