OLYMPUS DIGITAL CAMERA

Sponsored

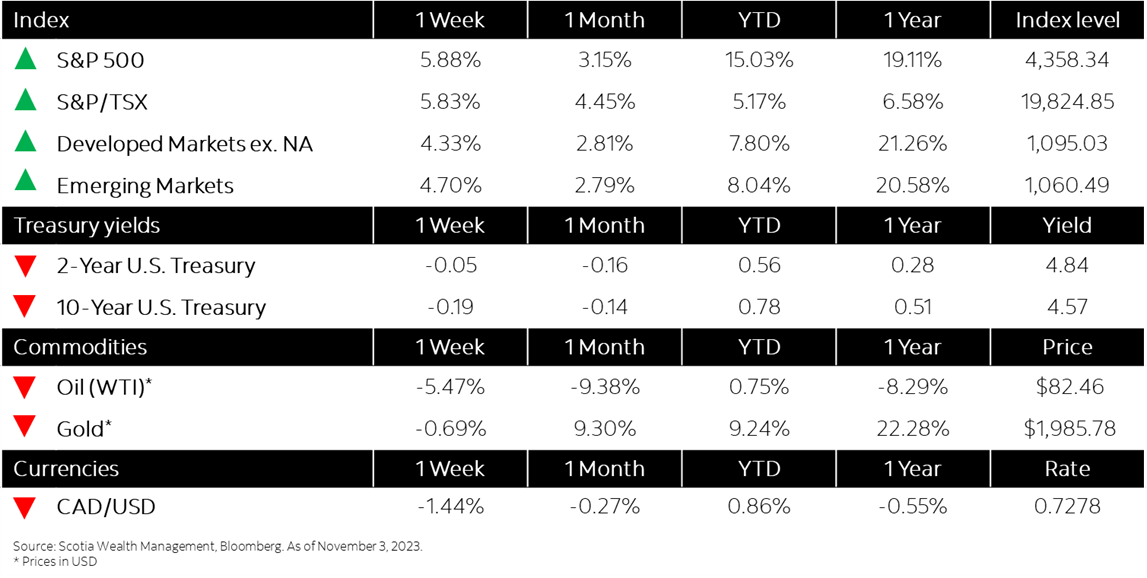

Market Watch: November 3

Nov 6, 2023 | 4:15 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Positive market sentiment pushes global indices higher

- Yields move lower following rate decision, employment data

- Canada’s economy flatlined in August, minor contraction seen in third quarter

- Fed extends pause on interest-rate hikes but keeps door open to higher rates

- Eurozone inflation drops sharply amid energy deflation, economic contraction

- In the news: Vaccine makers face write-offs as demand for pandemic products wanes