Sponsored

Market Watch: October 13

Oct 16, 2023 | 11:11 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

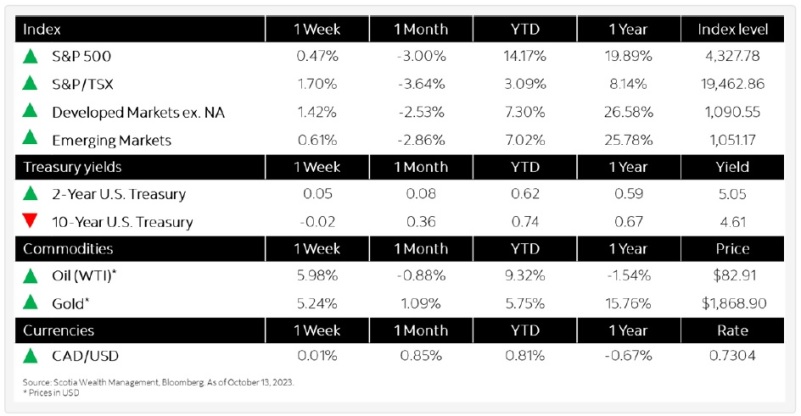

This week’s highlights

- Equity markets broadly positive following renewed inflation concerns

- Longer dated bond yields track slightly lower amid move to safe-haven assets

- Statistics Canada reports value of building permits up 3.4% in August to$11.9-billion

- Wholesale inflation in U.S. rises 2.2% in September, biggest year-over-year gain since April

- U.K. economy grew by 0.2% in August, but recession concerns remain

- In the news: Microsoft completes lengthy acquisition of Activision Blizzard,furthering industry consolidation

Week in review

Equity markets broadly positive following renewed inflation concerns