sponsored

Market Watch: Aug. 11, 2023

Aug 11, 2023 | 3:17 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

WEEK IN REVIEW

U.S. , INTERNATIONAL MARKETS EXPERIENCE SECOND WEEK OF LOSSES

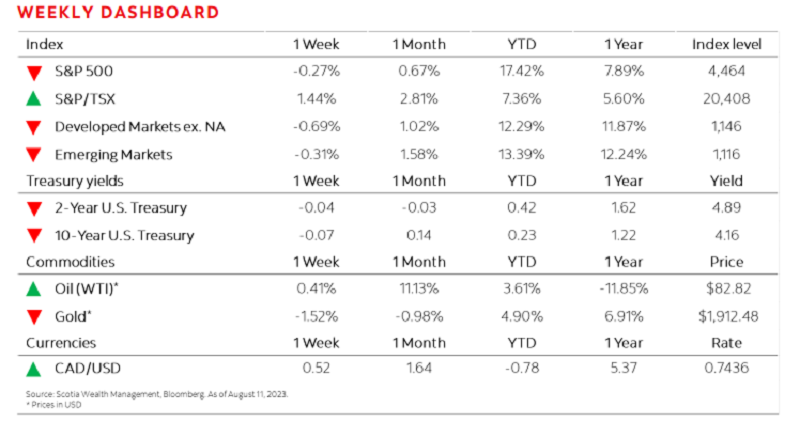

U.S. and international markets recorded a second week of losses after inching lower on Friday. Investors had to contend with a crosscurrent of corporate earnings which remain relatively strong as well as new inflation data. Much of the week’s market movements were in reaction to the inflation data, however. Investor sentiment was buoyed earlier in the week following the release of Consumer Price Index (CPI) data which came in lower-than-expected, pushing equity markets higher. Then, on Friday, the release of Producer Price

Highlights: