(Image Credit: Scotia Wealth Management)

Sponsored

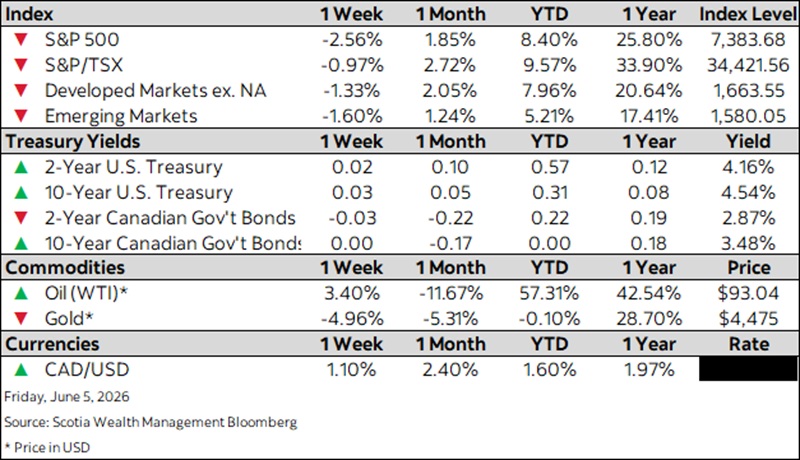

Market Watch — June 5, 2026

Jun 5, 2026 | 4:20 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Equity rally falters as investors weigh tighter policy conditions

- Strong labour data drives a late-week rates selloff

- Strong Canadian jobs data reinforce rate hike expectations

- Markets revisit expectations for Fed’s policy rate after U.S. labour data release

- Eurozone inflation reaccelerates as economic growth weakens