Sponsored

Market Watch – Dec. 12, 2025

Dec 12, 2025 | 4:20 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

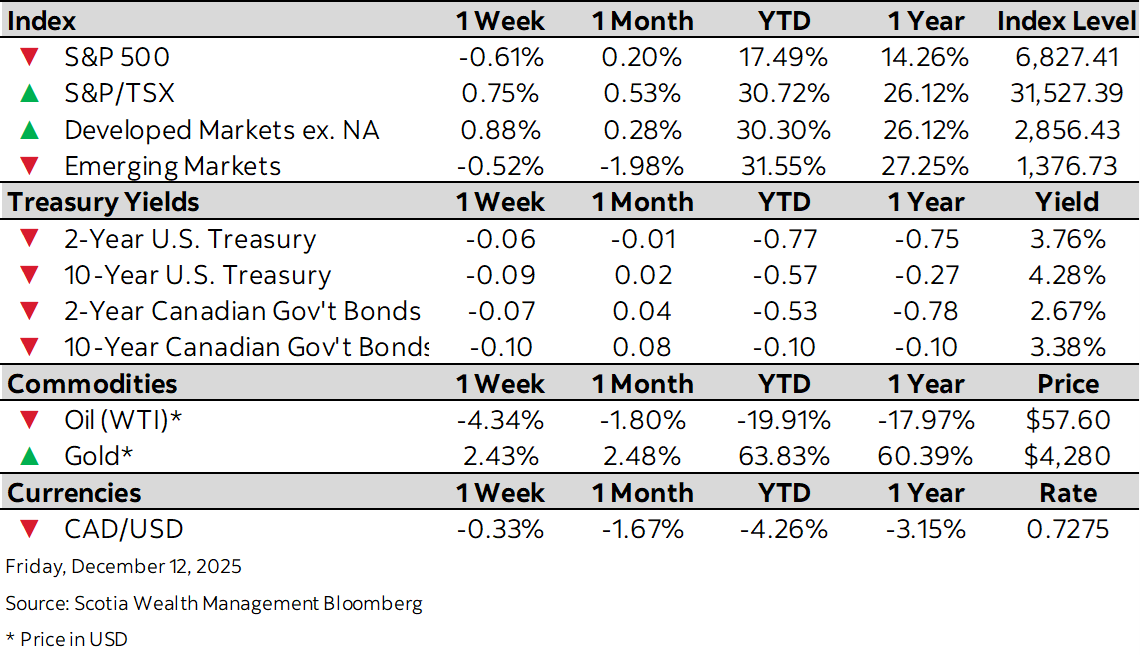

This week’s highlights

- Late week value rotation trims Fed interest rate cut gains

- Fed’s measured tone and BoC hold reinforce slower easing path

- Bank of Canada holds interest rate at 2.25% in last decision of 2025

- U.S. Federal Reserve cuts key rate by quarter-point, signals coming pause to cuts

- Eurozone economy posts stronger growth on investment rebound