OLYMPUS DIGITAL CAMERA

Sponsored

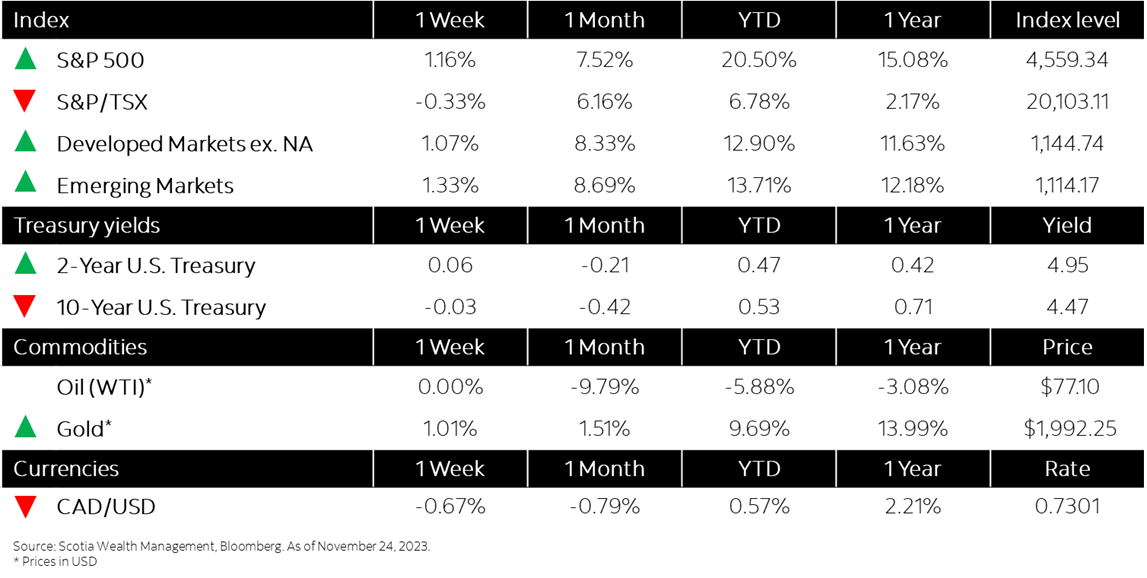

Market Watch: November 24

Nov 24, 2023 | 4:35 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Major indices rise for fourth straight week

- Treasury yields hit multi-month lows

- Canadian core and headline inflation decelerated in October

- U.S. initial unemployment claims decline by most since June

- Chinese advisors target steady growth in 2024, more stimulus

- In the news: OpenAI CEO fired and rehired within span of a week