Market Watch: July 28

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

WEEK IN REVIEW

Equity markets continue to deliver gains

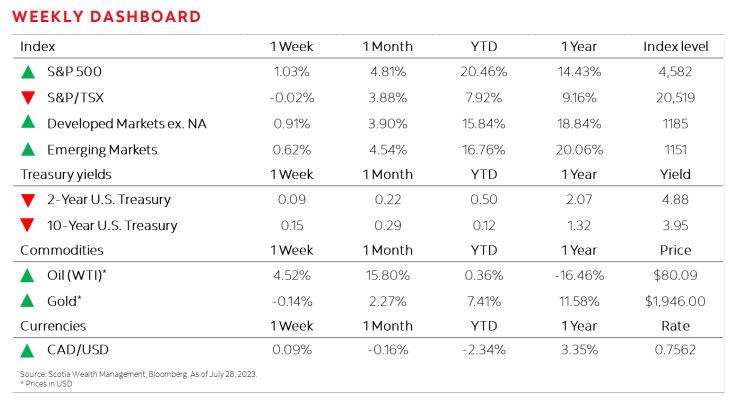

U.S. equities posted a third consecutive week of gains and returned 1.03 per cent1 on strong corporate earnings. Core personal consumption expenditures price index (PCE), a key inflation metric followed by the Federal Reserve (Fed), also fell to the lowest annual level in nearly two years. Canadian markets returned -0.02 per cent2 as key economic data indicated that the Canadian economy contracted in June. European markets marginally edged lower on Friday and posted a weekly gain of 0.91 per cent despite the European Central Bank (ECB) lifting rates 0.25 per cent, completing a third straight week of positive returns. Despite the growing geopolitical and growth risks, emerging markets closed 0.62 per cent4 for the week fuelled by real estate and consumer discretionary sectors.

Highlights: