(Image Credit: Scotia Wealth Management)

Sponsored

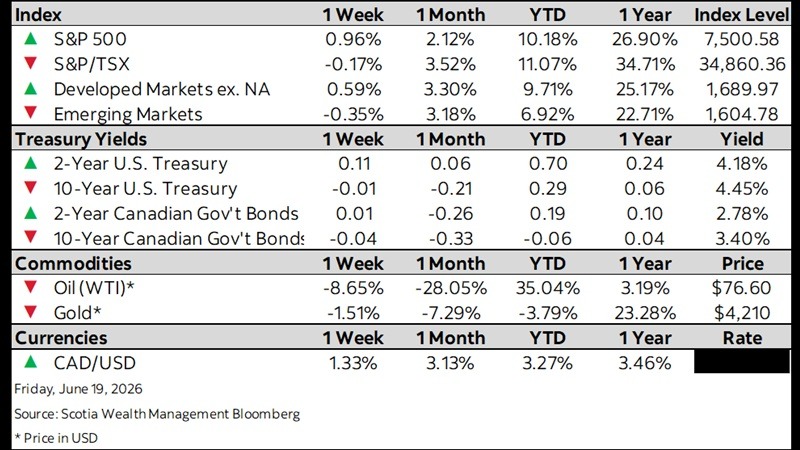

Market Watch — June 19, 2026

Jun 22, 2026 | 3:22 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Early optimism in equity markets gives way on hawkish shift in Fed tone

- Bond rally reverses amid central bank repricing

- Higher Canadian retail sales mask underlying weakness

- Fed’s hawkish reset puts rate cut hopes on hold

- Bank of England holds rates steady, balancing sticky inflation and soft growth