(Image Credit: Scotia Wealth Management)

Sponsored

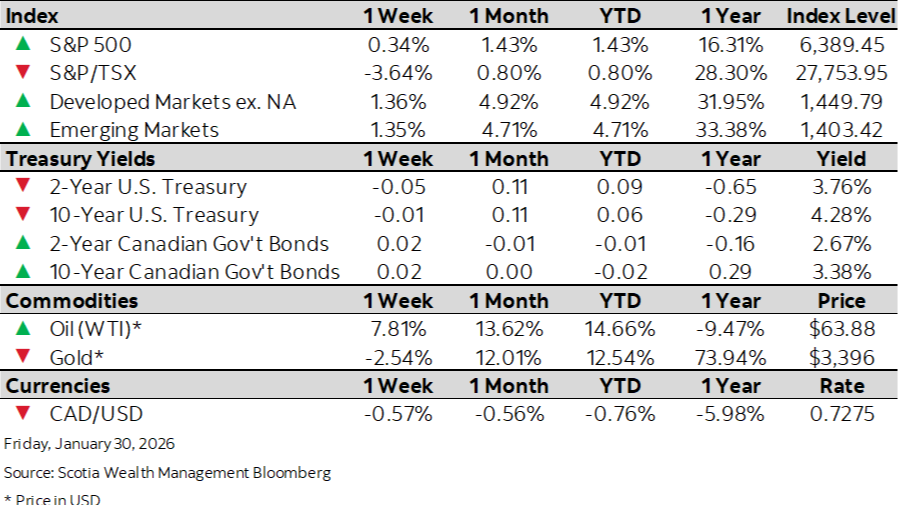

Market Watch: January 30

Feb 2, 2026 | 3:10 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Tech earnings gains tempered by policy uncertainty

- Sovereign curves anchored by Fed and BoC holds

- Bank of Canada holds benchmark interest rate steady amid trade uncertainty

- Federal Reserve holds rates steady, citing still-high inflation and solid growth

- Eurozone business confidence jumps at start of year