sponsored

Market Watch: April 18, 2025

Apr 21, 2025 | 9:34 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

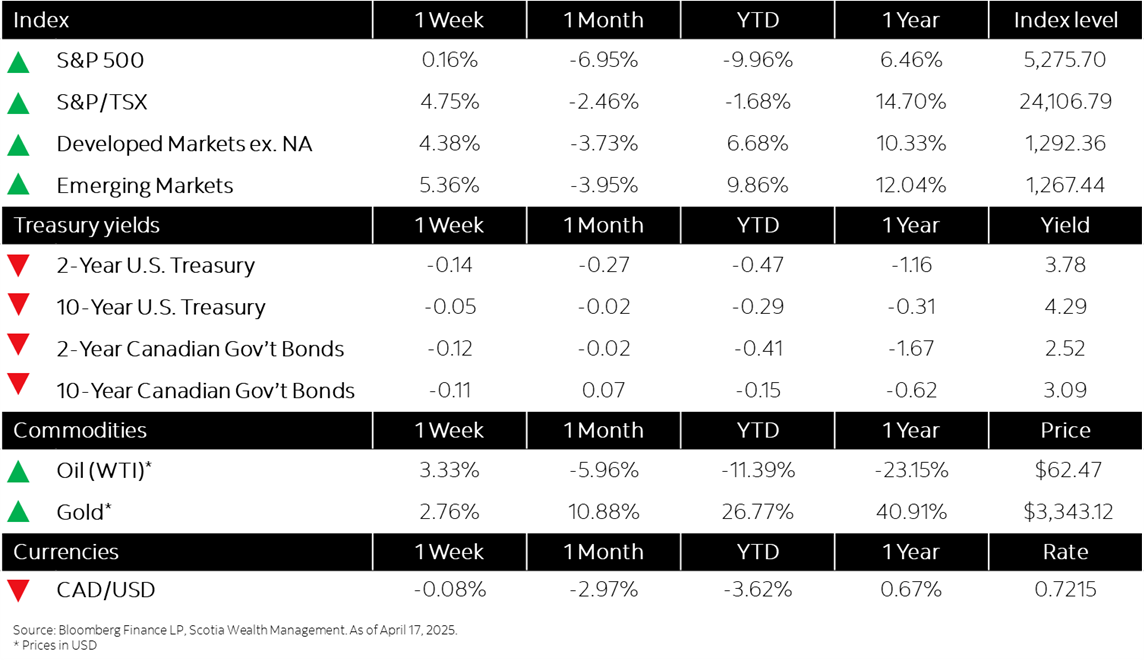

- Equity markets continue to show resiliency despite uncertainty

- Bond markets regain a more stable footing following several volatile weeks

- Bank of Canada holds rate steady at 2.75% amid trade war uncertainty

- U.S. retail sales surge in March due to motor vehicle purchases ahead of tariffs

- China’s exports surge as orders front-loaded before tariffs