SPONSORED

Market Watch: July 12, 2024

Jul 15, 2024 | 1:02 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

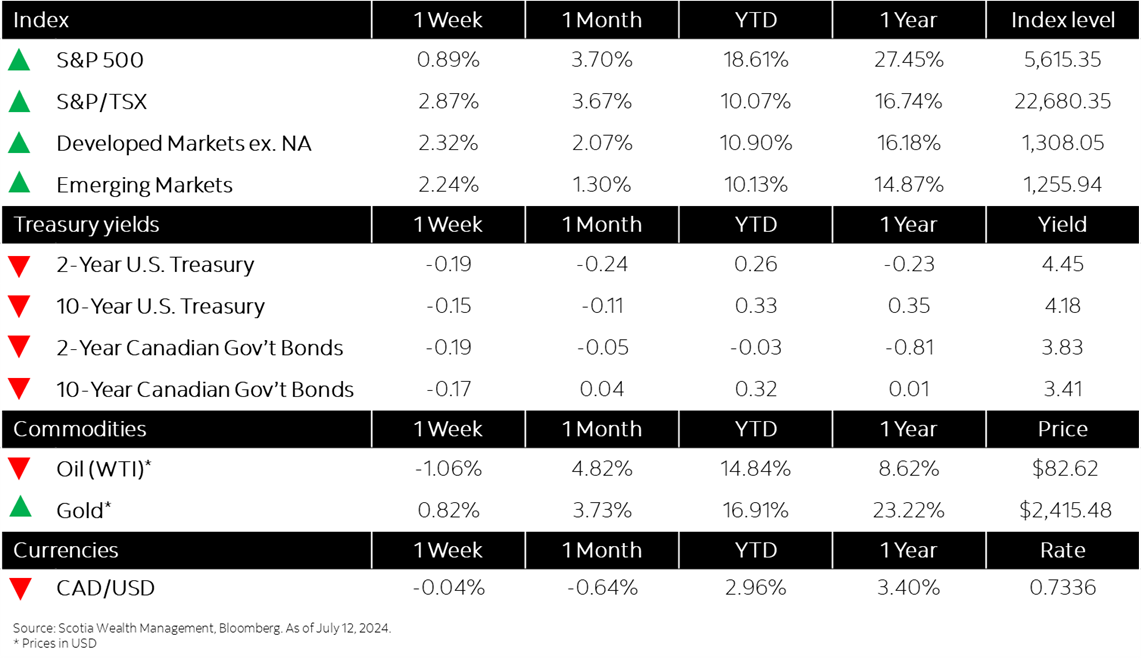

This week’s highlights

- Markets post fresh highs as U.S. inflation slows

- Bond yields move lower as disinflation momentum accelerates

- Average asking rents in Canada reached $2,185 in June as growth slows to 7 per cent

- U.S. inflation hits 3 per cent in June, lower than expected

- China consumer inflation stays tepid, factory-gate prices continue to fall

- In the news: U.S. imposes tariffs on non-Mexico origin metals

Week in review

Markets post fresh highs as U.S. inflation slows