Sponsored

Market Watch — July 3, 2026

Jul 4, 2026 | 10:44 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

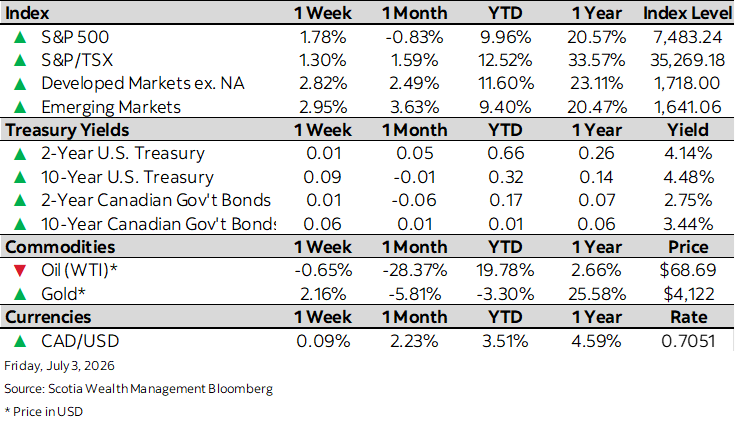

This week’s highlights

- Equity markets broadly positive amid short trading week for North America

- Bond markets lag as economic activity and moderating inflation encourage risk appetite

- Canada’s GDP rebounds while manufacturing remains in expansion mode

- Softer U.S. job gains ease pressure on U.S. Federal Reserve

- Eurozone inflation eases as labour market remains resilient