(Image Credit: Scotia Wealth Management)

sponsored

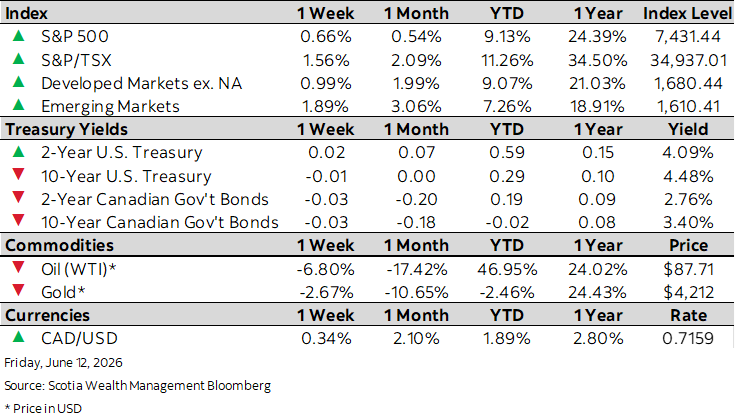

Market Watch — June 12, 2026

Jun 15, 2026 | 9:13 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

A summary of the week’s important events and how they could impact the market.

This week’s highlights

- Choppy week as inflation, geopolitics and AI trends collide

- Rates reprice on energy-driven inflation and policy outlooks before stabilizing

- Bank of Canada holds rate steady as it weighs weak growth against inflation risks

- Rising U.S. consumer prices increase odds of a Fed rate hike

- European Central Bank delivers first rate hike in nearly three years