sponsored

Market Watch – Aug. 9, 2025

Aug 11, 2025 | 2:08 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

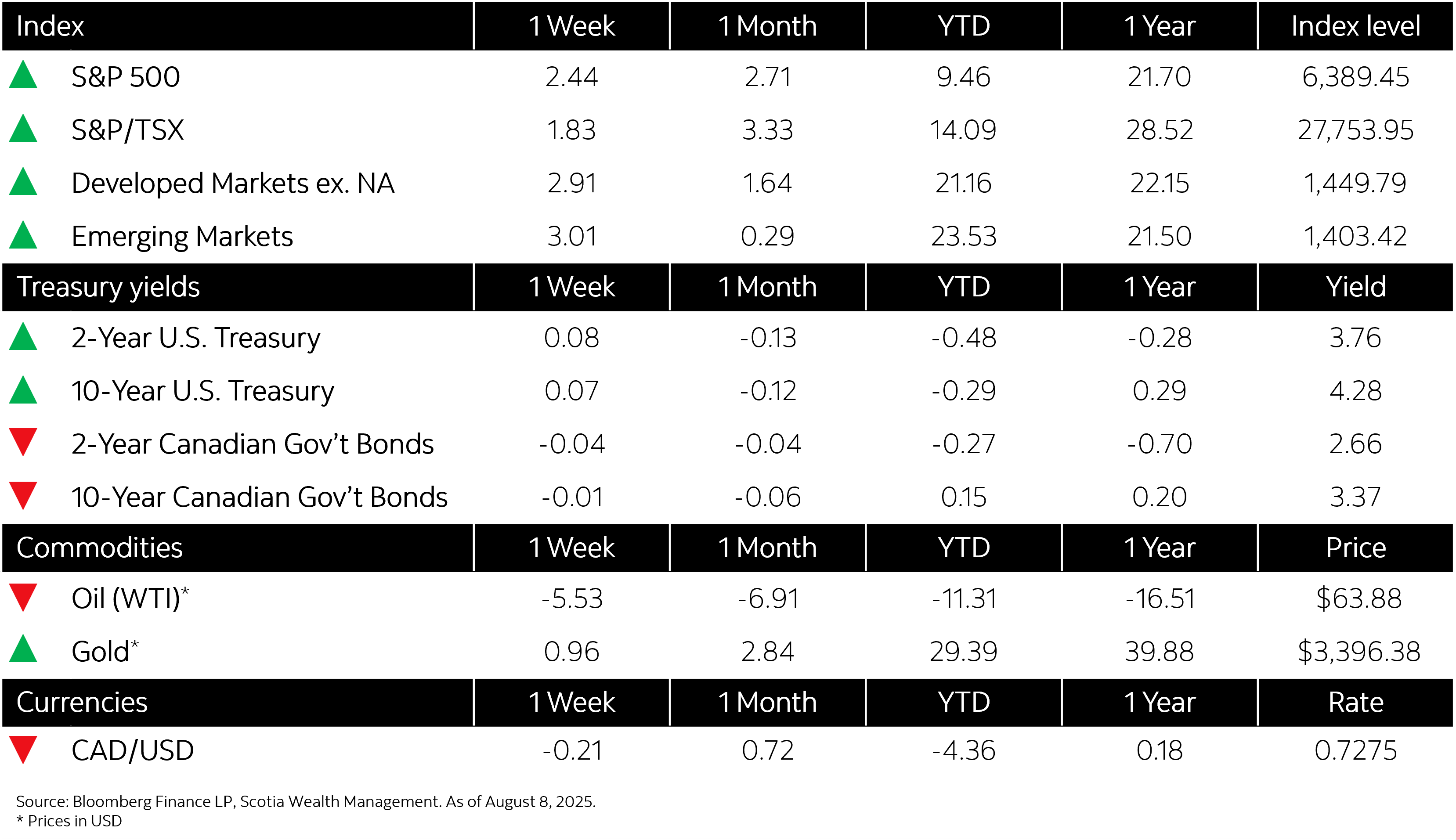

This week’s highlights

- Despite a mixed bag of events, economic data and tariffs news, markets end the week higher

- Weak jobs report pushes Canadian government bond rates lower, increases chances of Bank of Canada cut

- Canada’s trade deficit widened to $5.9 billion in June, second highest on record

- U.S. services sector PMI activity slows in July

- China’s services sector activity accelerates