sponsored

Market Watch: March 7, 2025

Mar 10, 2025 | 9:47 AM

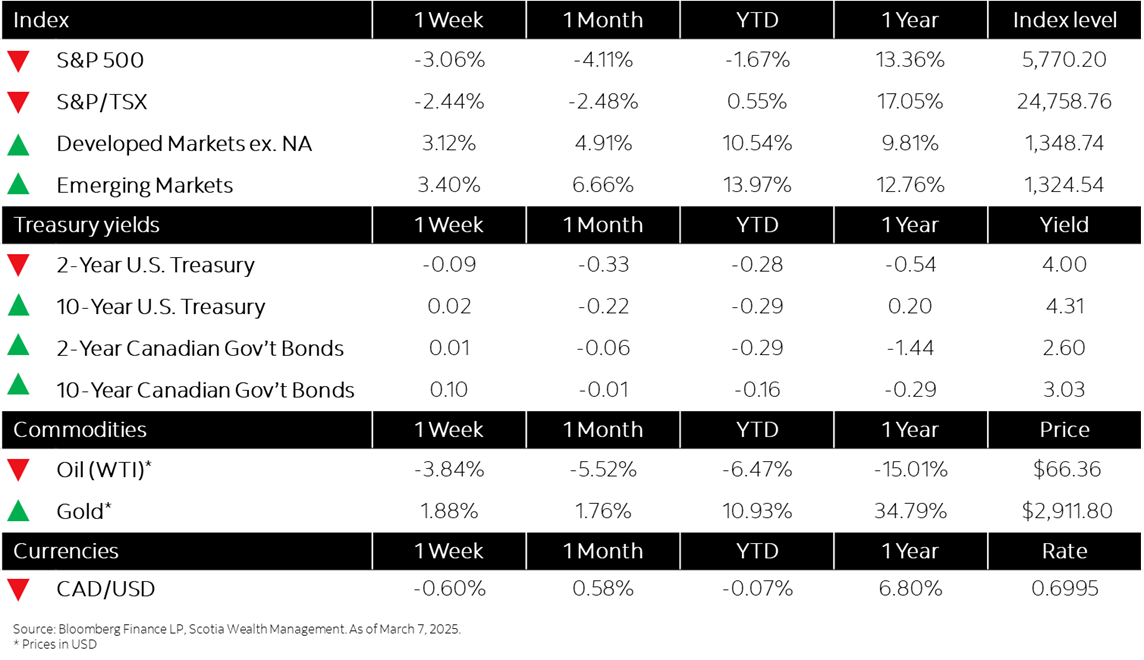

This week’s highlights

- North American markets experience worst week in six months

- Bonds falter amid volatile week of trading

- Canada’s trade surplus in January exceeds expectations, jumps to nearly $4 billion

- U.S. factory activity eased as tariffs threats spark accelerating costs

- ECB cuts rates to guard stalled economy against tariff threats

Week in review

North American markets experience worst week in six months