sponsored

Market Watch: Jan. 24, 2025

Jan 27, 2025 | 2:03 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

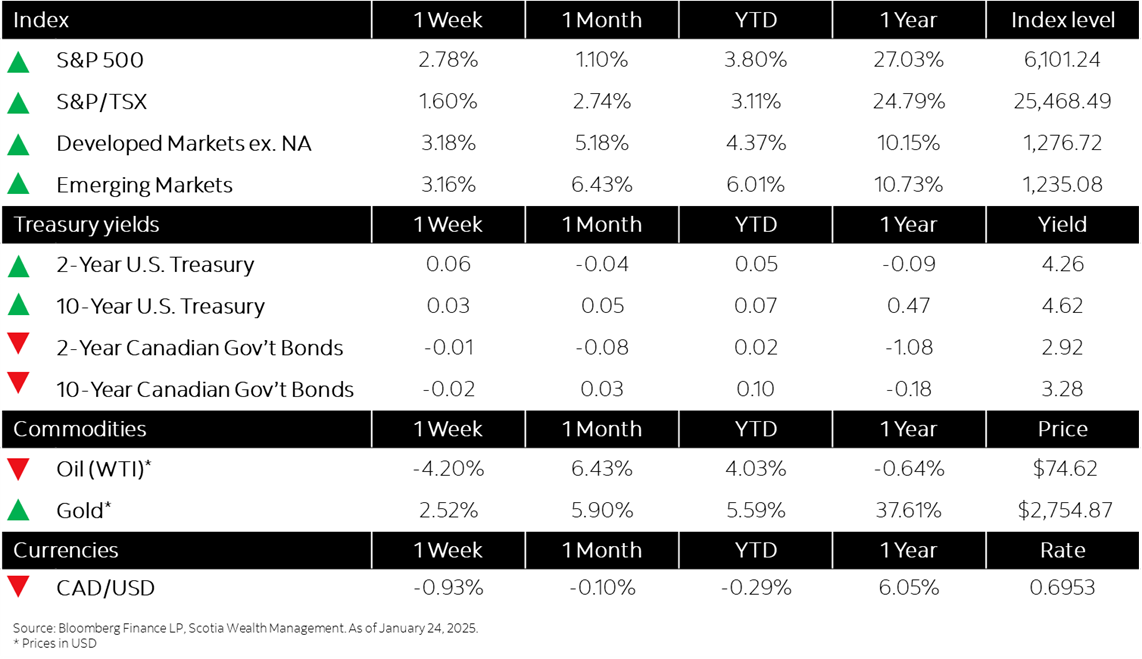

This week’s highlights

- Equity markets move higher even as trade and growth issues simmer

- Bond markets tread water amid interest rate uncertainty

- Canada’s annual inflation rate drops to 1.8% in December on sales tax relief

- IMF raises U.S. growth estimates

- U.K. jobs market weakens as BoE prepares to ease rates

Week in review

Equity markets move higher even as trade and growth issues simmer