sponsored

Market Watch: August 2, 2024

Aug 3, 2024 | 10:00 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

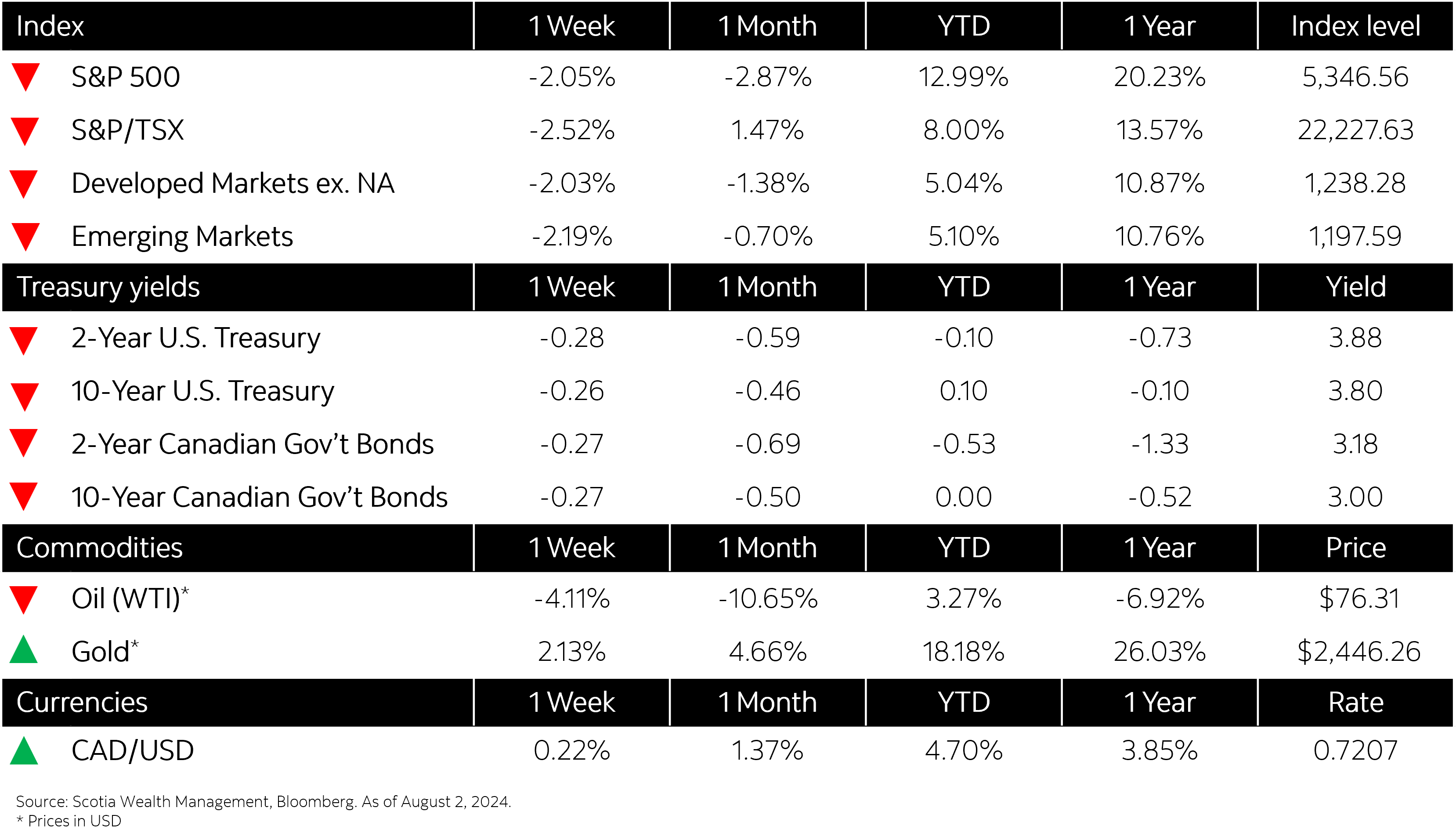

This week’s highlights

- Global markets fall as cooling labour data sparks slowdown concerns

- Bond yields fall as key data indicate a softer labour market

- Canada’s GDP likely to surpass central bank’s second-quarter forecast

- U.S. Fed clears path for September rate cut

- Eurozone inflation picks up pace in blow to rate-cut hopes

- In the news: OPEC+ sticks to output cuts while signalling possible future increases