Sponsored

Market Watch: January 12

Jan 16, 2024 | 3:30 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

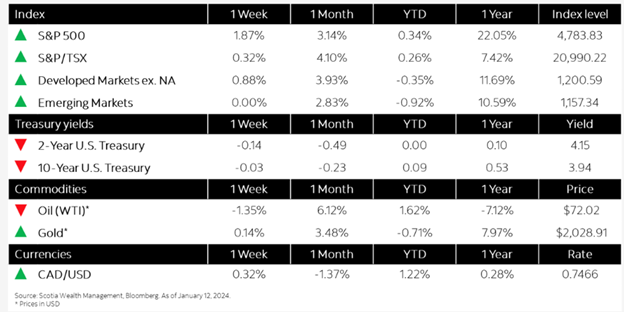

This week’s highlights

- Bank earnings buoy markets amid geopolitical events and inflation readings

- Sovereign yields move lower, strong demand for investment grade credit

- Canada’s trade surplus narrowed in November as imports rose on nuclear fuel

- U.S. inflation edged up in December after rapid cooling most of 2023

- Eurozone inflation rises less than expected

- In the news: First of its kind Bitcoin ETF approved by regulators

Week in review

Bank earnings buoy markets amid geopolitical events and inflation readings