Sponsored

Market Watch: November 10

Nov 12, 2023 | 4:08 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

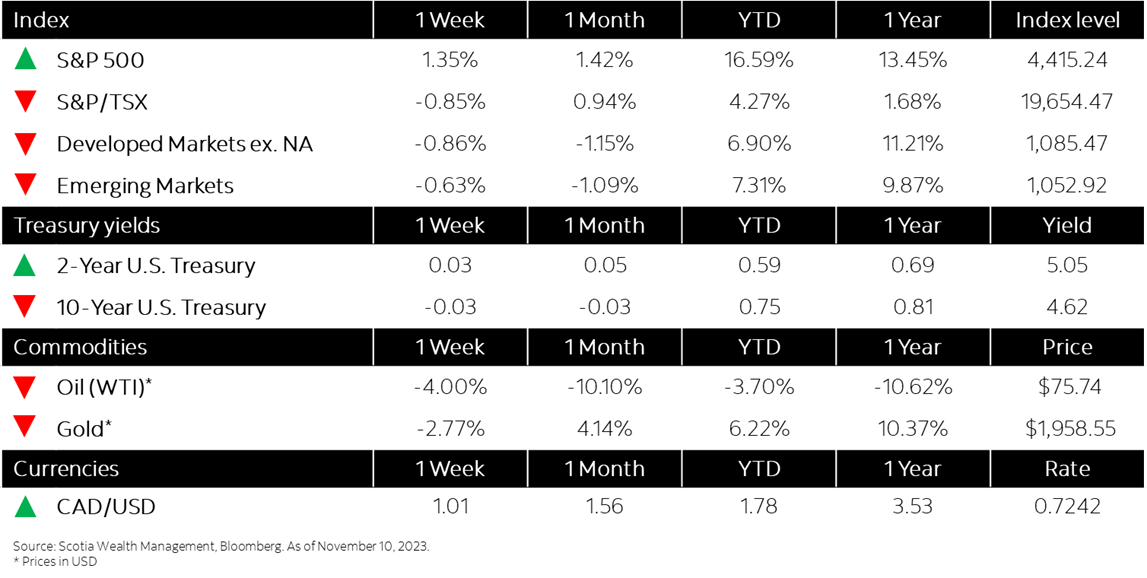

This week’s highlights

- Stocks extend weekly gains following bond market tumult

- Sovereign yields flat in wake of weak 30-year Treasury auction

- Canada’s trade surplus doubled to $2.04-billion in September on energy price surge

- U.S. lending standards tightened further in 3Q

- China’s exports tumble again in fresh sign of economic trouble

- In the news: Office-sharing company WeWork files for bankruptcy protection

Week in review

Stocks extend weekly gains following bond market tumult