(Supplied)

Sponsored

Market Watch: September 15

Sep 18, 2023 | 12:23 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

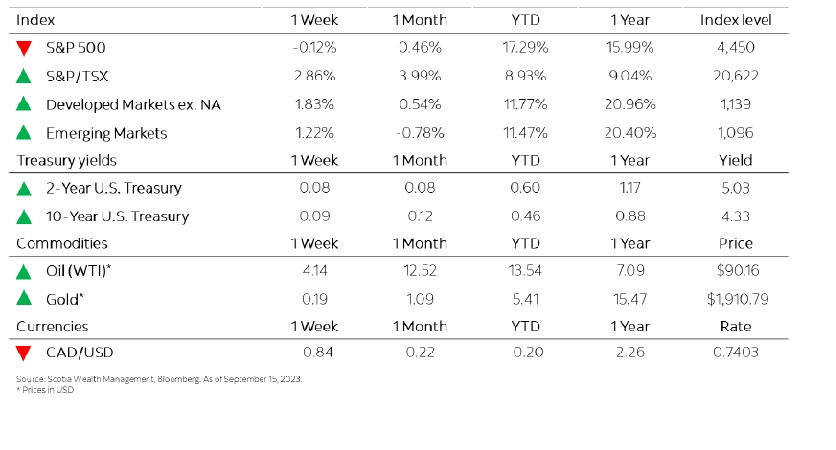

WEEK IN REVIEW

GLOBAL SENTIMENT BOOSTED DESPITE MIXED ECONOMIC DATA

Though equities continued to demonstrate volatility as key domestic and global economic data released this week gave mixed signals, major indices posted a positive return. The overall global sentiment was boosted due to stronger than expected industrial production, retail sales and inflation data from China after the government increased its efforts to stimulate the world’s second largest economy. U.S. equity markets were steady throughout the week but were perturbed Friday as investors digested a fresh batch of economic data which also coincided with a ‘triple witching’ event.

Highlights: