OLYMPUS DIGITAL CAMERA

Sponsored

Market Watch: July 14

Jul 17, 2023 | 3:01 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

WEEK IN REVIEW

Strong earnings, low inflation set the stage for risk asset rally

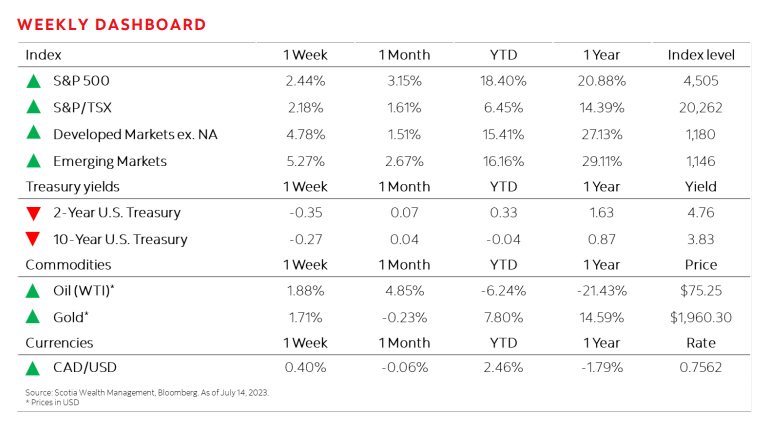

U.S. equities returned 2.44 per cent1 following a spate of strong earnings and low inflation in June, while Canadian equities seemed unfazed by yet another rate hike from the Bank of Canada (BoC), returning 2.18 per cent2. Developed markets, like North America for example, and emerging markets were by far the best-performing regions for the week returning 4.78 per cent3 and 5.27 oer cent4, respectively. European markets – which had their best week since March – rallied along with other risk assets as U.S. inflation eased, riding a wave of optimism that the U.S. Federal Reserve (Fed) may be near the end of its tightening cycle.

Highlights: