sponsored

Market Watch – Oct. 24, 2025

Oct 27, 2025 | 10:15 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Equity markets swing as CPI data and PMI divergence shape rate expectations

- Rates ease on softer U.S. CPI while credit markets stay resilient

- Canada’s inflation rate rises to 2.4% in September, StatCan reports

- U.S. home sales in September rose, boosted by falling mortgage rates

- China’s economy expands at slowest pace in a year

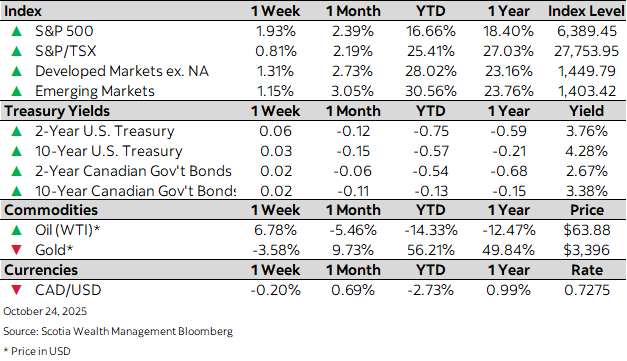

Week in review

Equity markets swing as CPI data and PMI divergence shape rate expectations