Sponsored

Market Watch: July 11, 2025

Jul 14, 2025 | 1:26 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

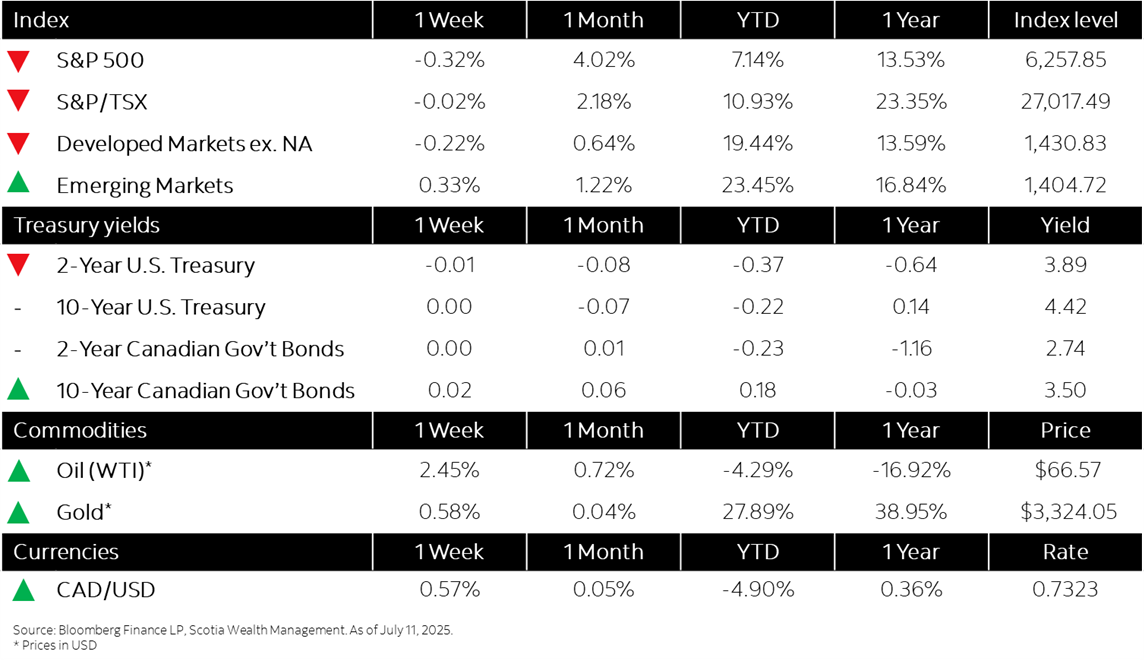

This week’s highlights

- Tariff volatility and mixed FOMC views reinforce investors’ cautious outlook

- Rates muted on trade uncertainty and resilient economic data while credit holds firm

- Canada’s economic activity reaches four-month high in June

- U.S. small business sentiment darkens slightly

- German exports fall again as tariffs drag on economy

Week in review

Tariff volatility and mixed FOMC views reinforce investors’ cautious outlook