SPONSORED

Market Watch: November 1

Nov 1, 2024 | 5:05 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

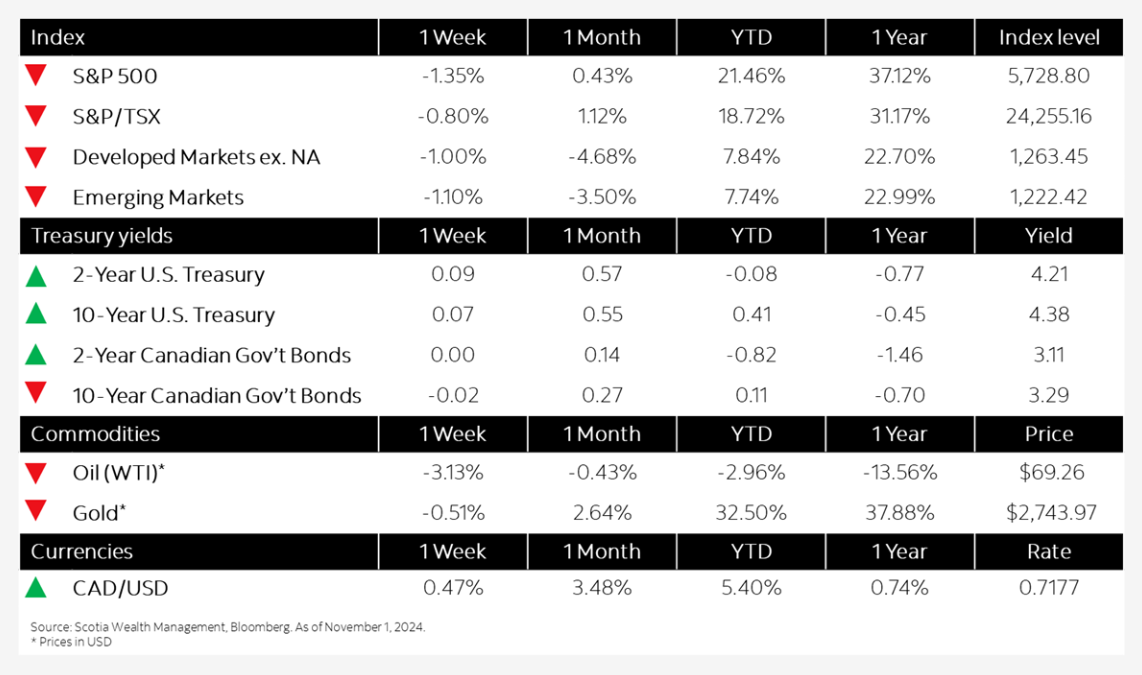

This week’s highlights

- Rate sensitive sectors pull broader index lower

- Bond market continues to see volatility amid fluctuating interest rate forecasts

- Canada’s economy stalled in August, likely grew 0.3% in September

- U.S. economic growth extends solid streak

- Eurozone expands faster than expected, raising hopes of soft landing

- In the news: Energy needs of AI could drive resurgence in nuclear power

Week in review

Rate sensitive sectors pull broader index lower