Market Watch: September 27, 2024

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

Week in review

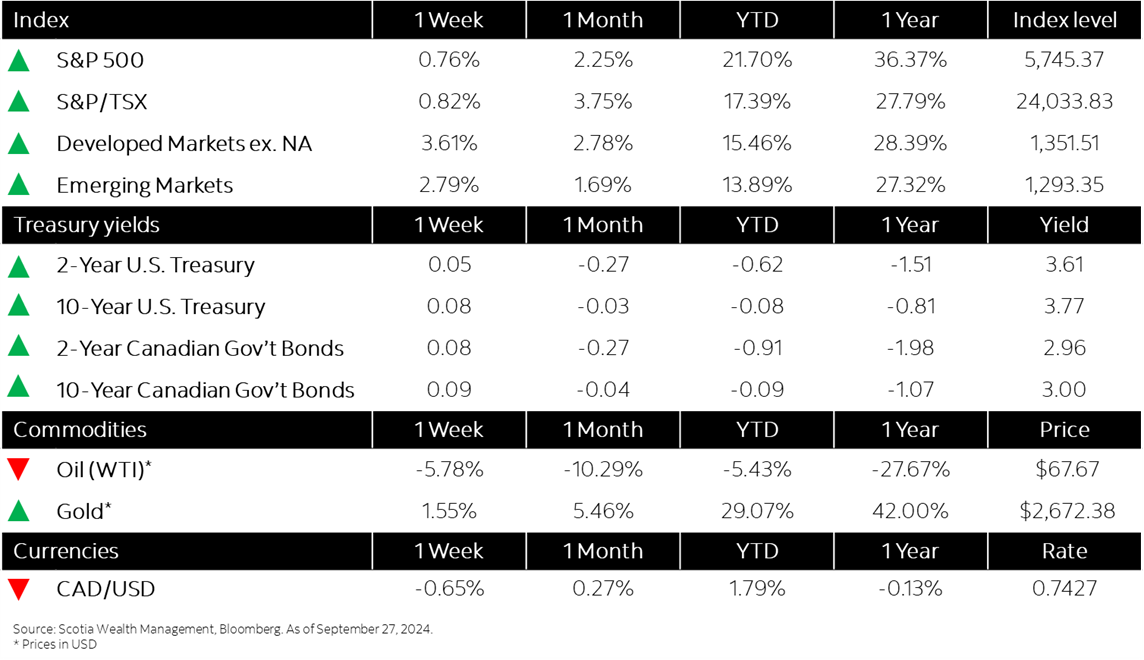

Equity markets move higher despite mixed economic data

Equity markets experienced mixed performance for the week but closed in positive territory. U.S. equities remained stable, reaching new record highs early in the week, while Chinese stocks rallied following the People’s Bank of China’s (PBoC) comprehensive stimulus package. However, European equities faced challenges, with a contraction in business activity and confidence weighing on sentiment. Midweek, U.S. equity futures rose on expectations of further fiscal stimulus from China and potential easing by the U.S. Federal Reserve (Fed) and the European Central Bank (ECB). By week’s end, U.S. equities saw slight gains after the Federal Reserve’s preferred inflation measure aligned with expectations, while European stocks benefited from declining inflation expectations in the Eurozone.

Highlights: