SPONSORED

Market Watch: August 23

Aug 26, 2024 | 2:06 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Equity markets close out another strong week

- Bonds rally following Powell comments at Jackson Hole

- Canada’s inflation rate drops to slowest pace in three years

- U.S. nonfarm payrolls revised lower

- China maintains key loan rates amid signs of economic recovery.

- In the news: First-of-its-kind Canadian rail strike affects key supply chains

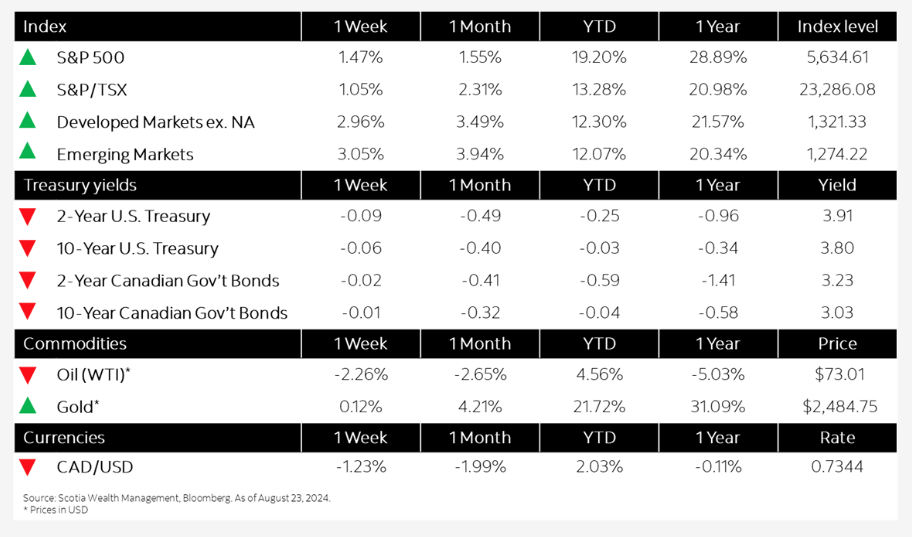

Week in review

Equity markets close out another strong week