SPONSORED

Market Watch: June 28

Jul 2, 2024 | 3:52 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

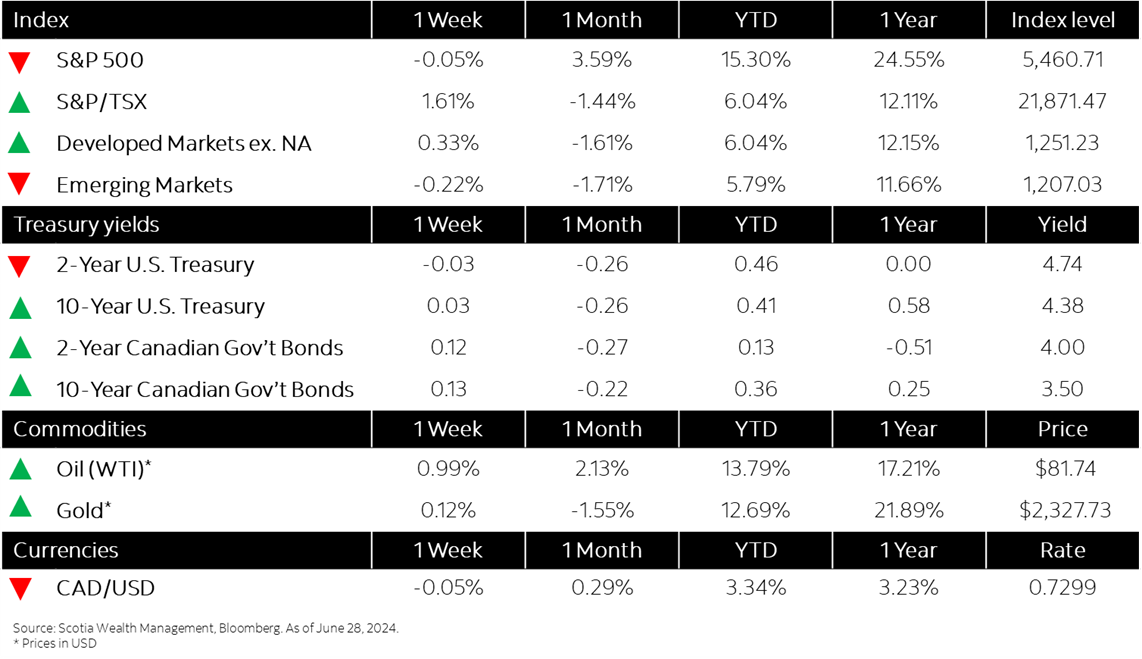

This week’s highlights

- Markets wrap productive first half of 2024

- Bond yields flat despite positive PCE reading

- Canada’s inflation rate accelerated to 2.9% in May

- U.S. economic growth for last quarter revised up to a 1.4% annual rate

- German business sentiment weakens with economic, political clouds ahead

- In the news: Global shipping rate surge could lead to higher costs and inflation

Week in review

Markets wrap productive first half of 2024