Sponsored

Market Watch — March 20, 2026

Mar 20, 2026 | 4:37 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

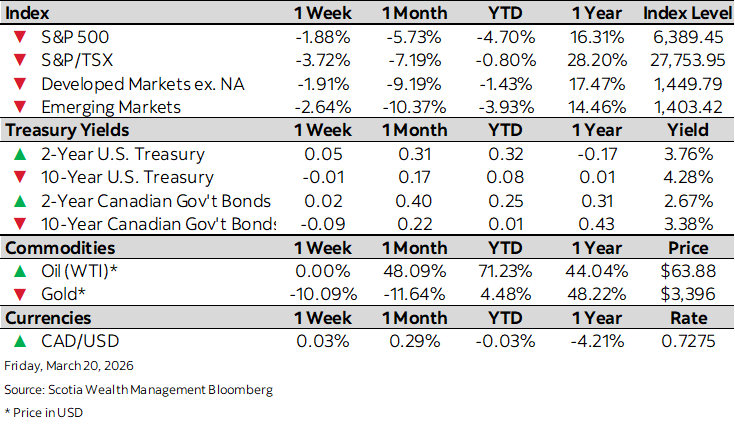

This week’s highlights

- Equities continue to struggle as energy shock causes a reassessment of policy path

- Hotter inflation expectations push front-end yields sharply higher

- Bank of Canada keeps key interest rate at 2.25% amid oil-driven inflation risks

- U.S. Federal Reserve holds rates steady, projects single rate cut for 2026

- China’s economy off to steady start in 2026 amid lowered expectations