(Image Credit: Scotia Wealth Management)

Sponsored

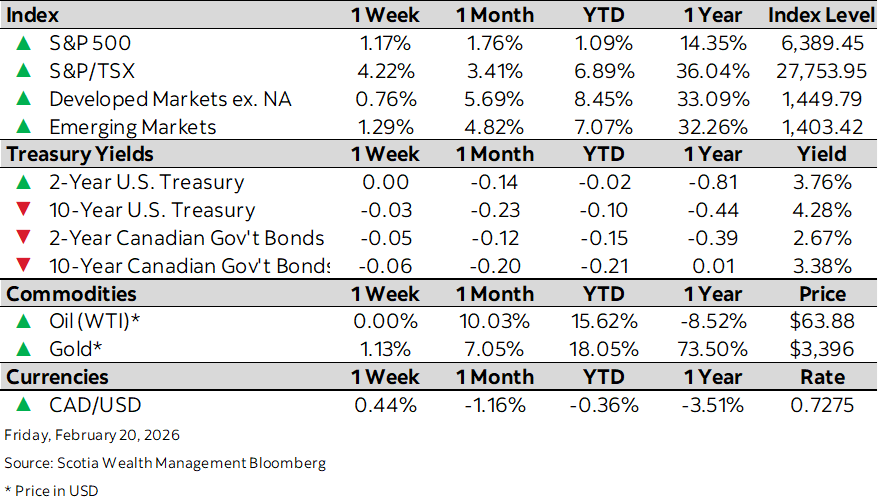

Market Watch: February 20

Feb 23, 2026 | 3:06 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Equities seek direction amid flurry of mixed data, policy, and geopolitical news

- Sovereign yields converge on mixed economic data and shifting policy expectations

- Canada’s annual inflation rate edges down in January as gasoline costs drop

- U.S. Q4 GDP up just 1.4%, missing estimate; inflation firms at 3%

- Europe’s exports to U.S. fell as imports from China rose