(Image Credit: Scotia Wealth Management)

Sponsored

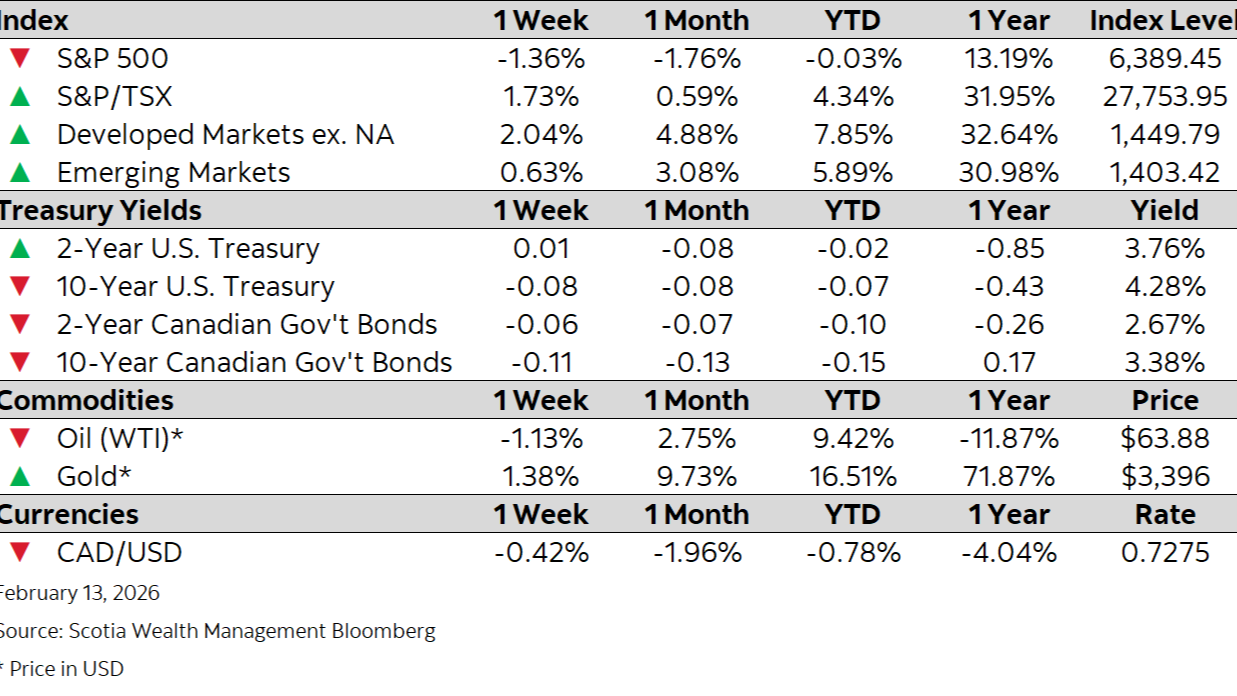

Market Watch: February 13, 2026

Feb 17, 2026 | 4:04 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Markets remain resilient despite AI pressures continuing to ripple though global markets

- Cooler U.S. inflation continues bond rally

- Canada building permits rebound in December

- U.S. adds 130,000 jobs in January, beating expectations

- China’s consumer inflation eases, producer prices stay in decline