sponsored

Market Watch – Dec. 5, 2025

Dec 8, 2025 | 12:49 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

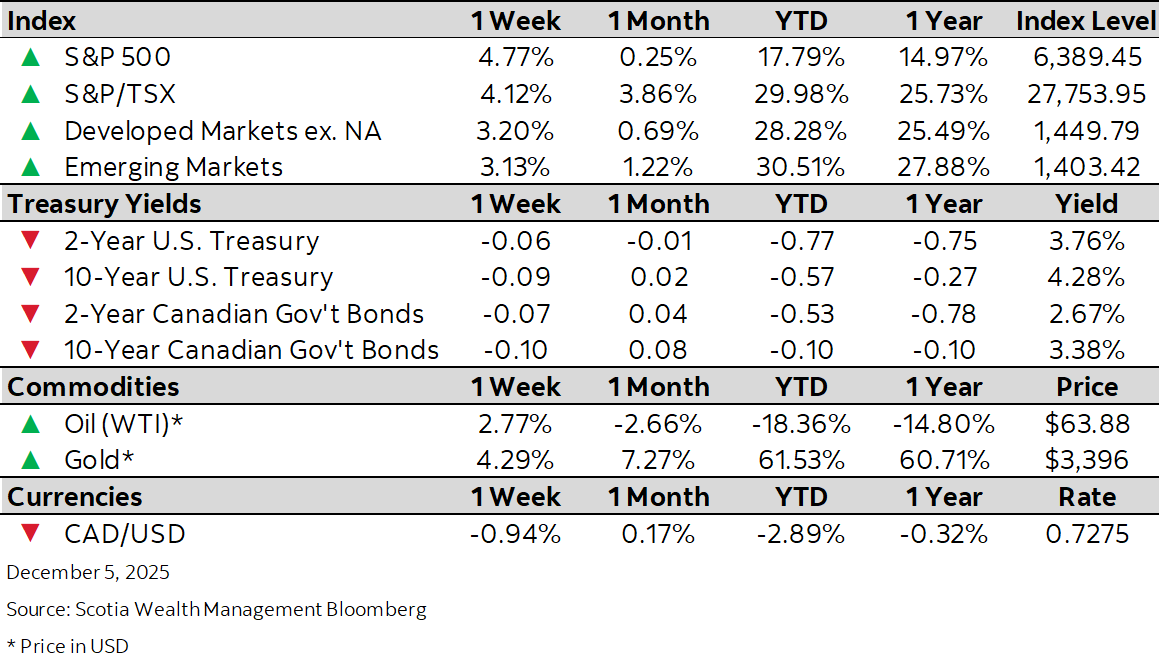

This week’s highlights

- Mid-week sentiment surge moves equity markets into positive territory

- Divergent policy signals drive rate swings

- Canada’s unemployment rate falls to 6.5%, driven by rise in part-time work

- U.S. manufacturing contracts for ninth straight month

- China’s manufacturing gauge shows slightly firmer growth momentum