Sponsored

Market Watch: November 28

Dec 1, 2025 | 11:51 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

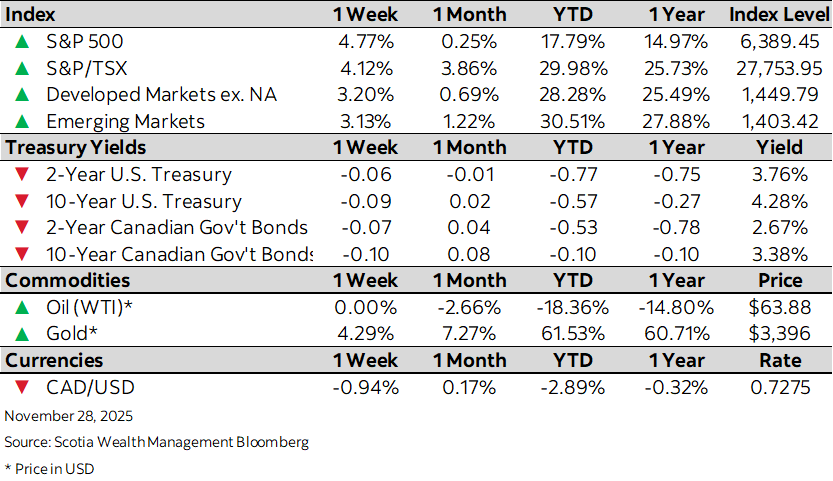

This week’s highlights

- Tech strength and FOMC rate cut bets drive steady equity gains despite releases of stale economic data

- Bond markets juggle fiscal discipline and inflation uncertainty

- Canada reports third-quarter GDP growth of 2.6%, avoiding recession

- U.S. producer prices rise in September on higher energy costs

- Eurozone business activity continues growth despite manufacturing hit