sponsored

Market Watch – Aug. 29, 2025

Aug 30, 2025 | 11:15 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

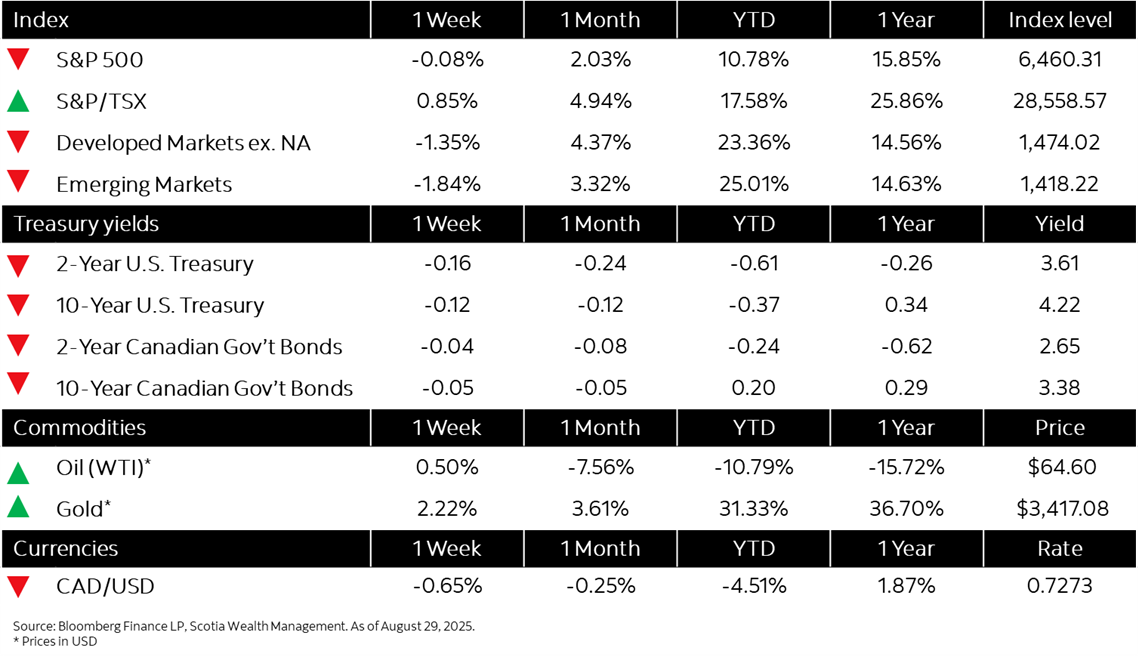

This week’s highlights

- Markets diverge on dovish central bank signals and mixed growth and inflation data

- Yields shift as central banks lean towards easing amid data uncertainty

- Canada’s economy contracts more than expected in second quarter as tariffs hit exports

- U.S. reports solid July consumer spending, core inflation firmer

- German consumers feel ever gloomier as economy slumps