sponsored

Market Watch – Aug. 22, 2025

Aug 25, 2025 | 10:05 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

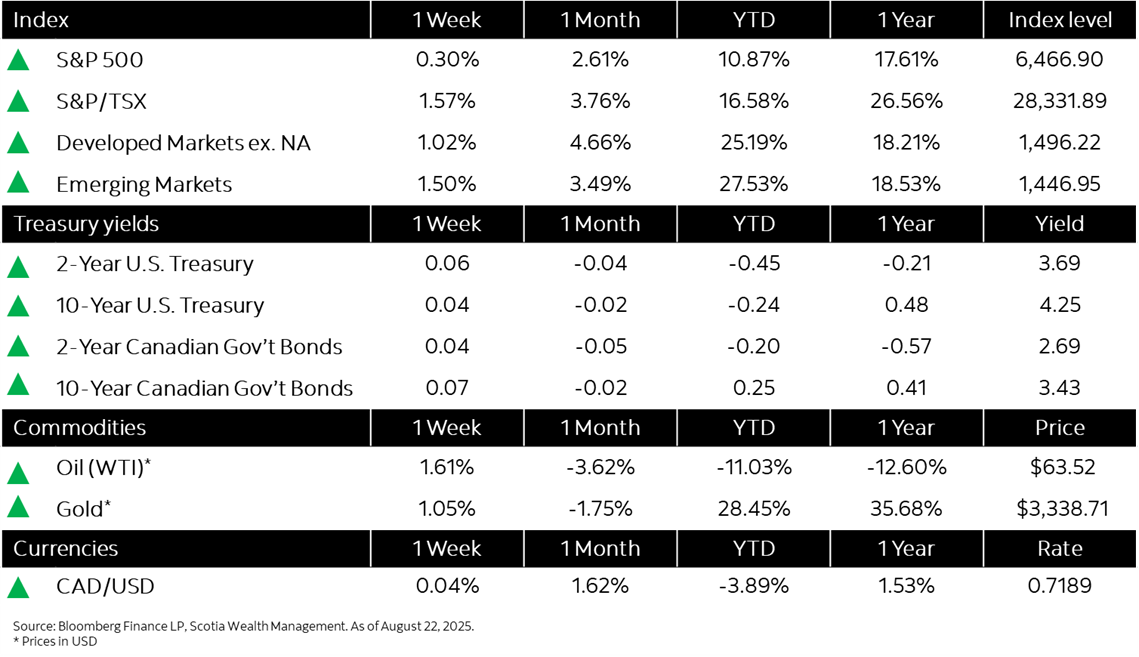

- Equities mixed for the week as policy signals and PMI data drive volatility across regions

- Rates stabilize on inflation and policy cues

- Canada’s inflation rate slows to 1.7% in July, led by falling gasoline prices

- U.S. housing starts tick higher in July, led demand for rental housing

- European trade takes fresh tariff hit as U.S. exports slump