Sponsored

Market Watch: July 4, 2025

Jul 4, 2025 | 4:21 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

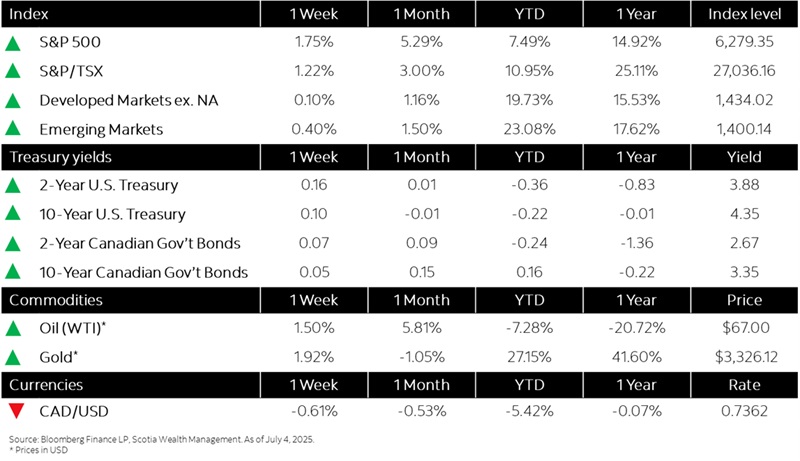

- Markets close higher despite tariff threats tempering labour-driven gains

- Labour strength and tariff tensions steepen curves

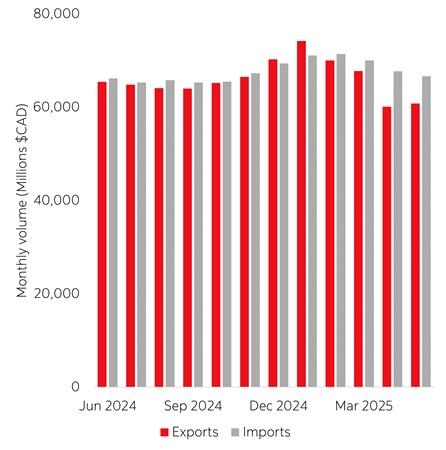

- Canada’s trade deficit narrows in May, exports to U.S. decrease for fourth straight month

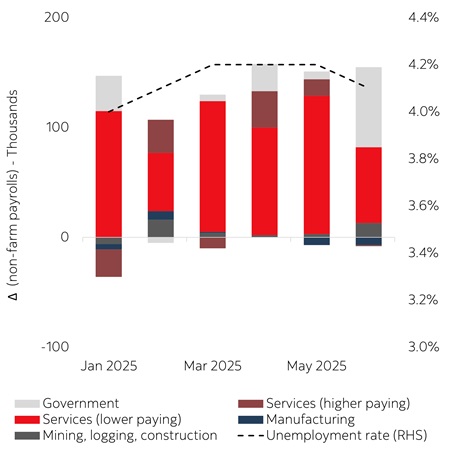

- Steady hiring added 147,000 jobs to U.S. economy in June

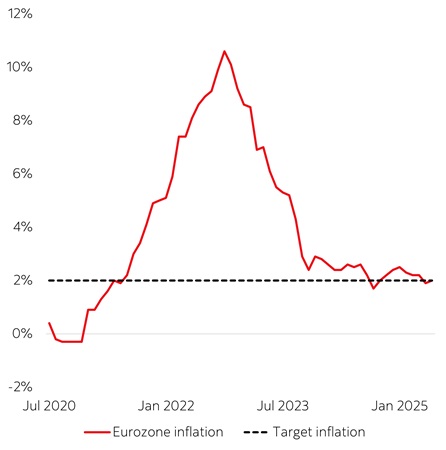

- Eurozone inflation hits 2% target, raising chance of ECB rate hold