sponsored

Market Watch: June 27, 2025

Jun 30, 2025 | 10:11 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

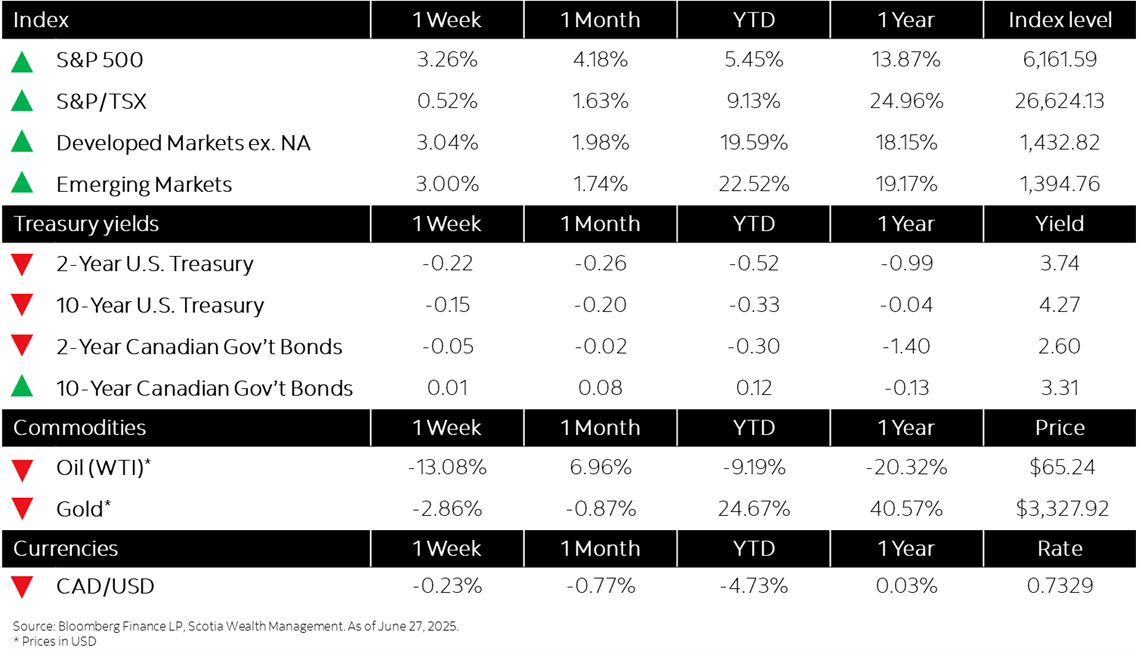

This week’s highlights

- Markets advance as Mideast geopolitical tensions ease despite cautious tone from Fed

- Bond yields relatively steady amid data surprises complicating the monetary policy outlook

- Canadian May inflation holds steady at 1.7% as economy shrinks

- U.S. consumer spending falls in May while prices tick up

- German business sentiment climbs as expectations brighten