sponsored

Market Watch: May 9, 2025

May 9, 2025 | 4:26 PM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

This week’s highlights

- Equity markets show cautious optimism amid evolving trade deal discussions

- Rates move higher following policy decisions by Central Banks

- Canada’s trade deficit narrows more than expected in March as imports fall

- U.S. Federal Reserve holds rates steady, cites rising risk of higher inflation and unemployment

- China services sector gauge slips to seven-month low amid trade spat

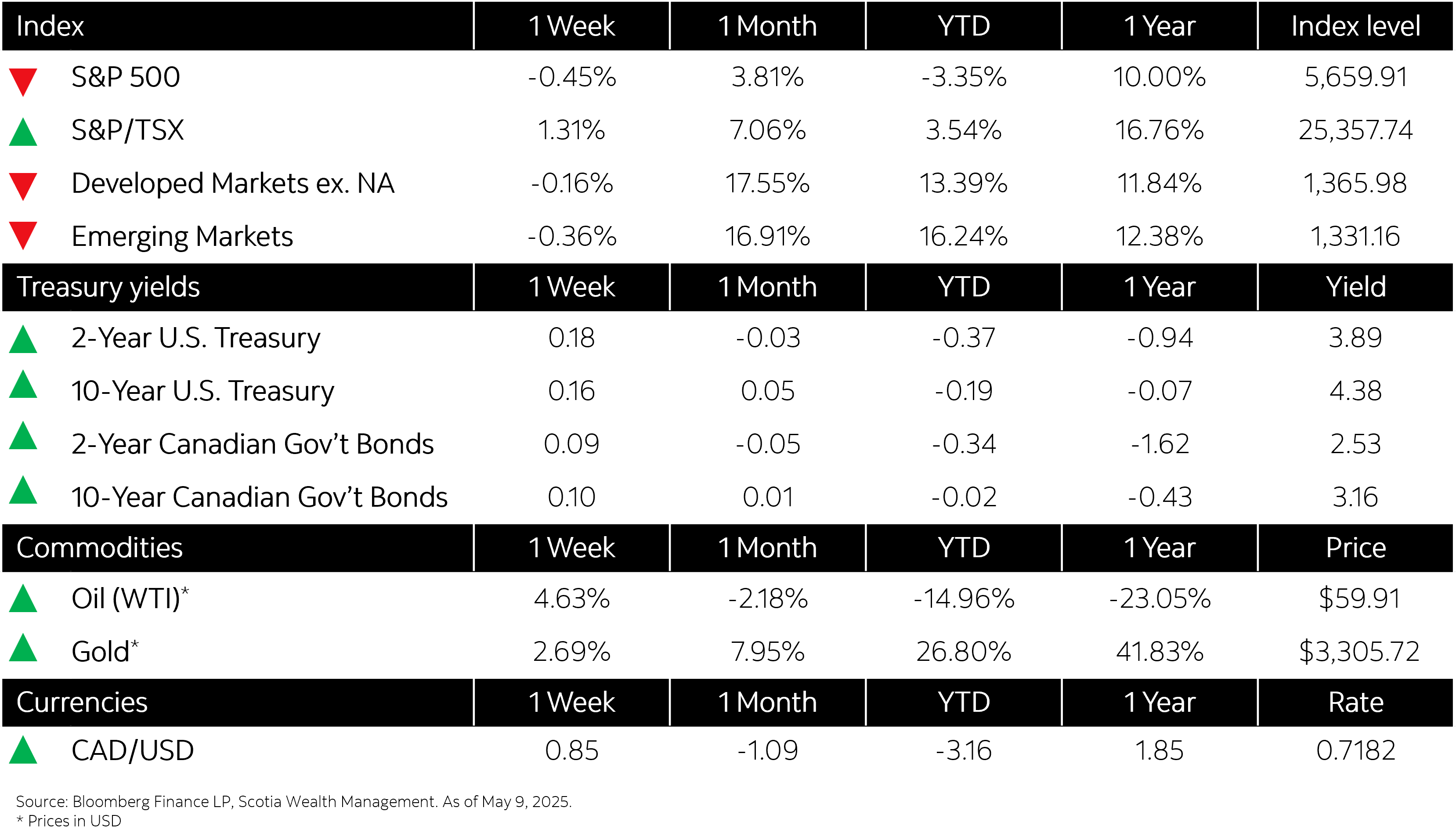

Week in review

Equity markets show cautious optimism amid evolving trade deal discussions