SPONSORED

Market Watch: March 14

Mar 17, 2025 | 10:12 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

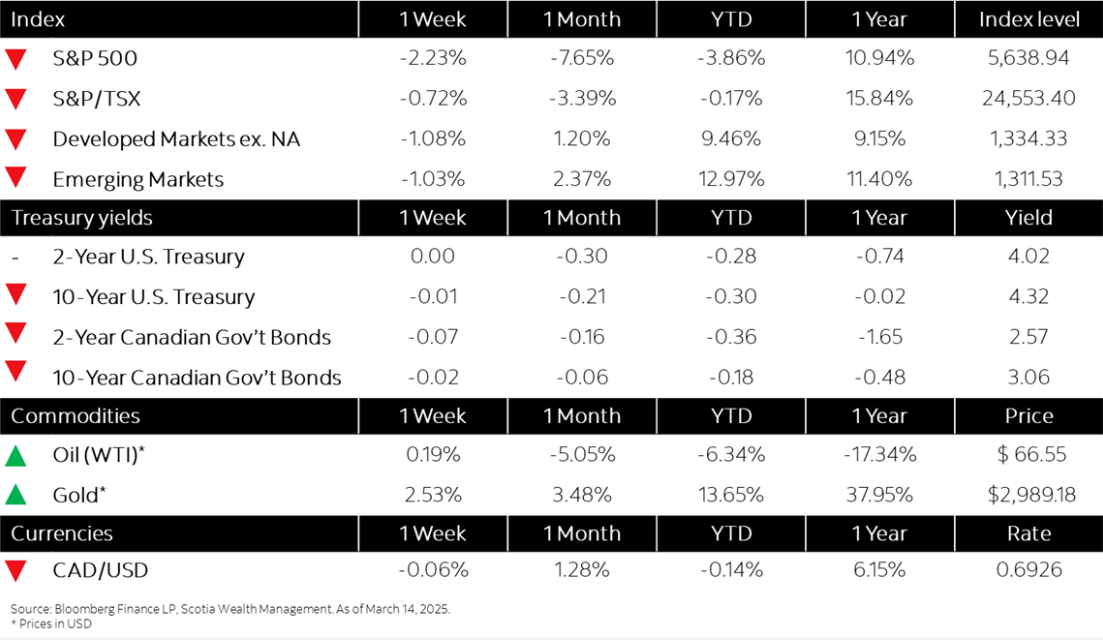

This week’s highlights

- North American markets continue to recede amid trade turmoil

- Bonds benefit from safe haven flows

- Bank of Canada cuts key rate to 2.75% as trade war rattles economy

- U.S. inflation hit 2.8% in February, less than expected

- German industrial production rose at start of 2025

Week in Review

North American markets continue to recede amid trade turmoil