sponsored

Market Watch: Jan. 13, 2025

Jan 13, 2025 | 9:57 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

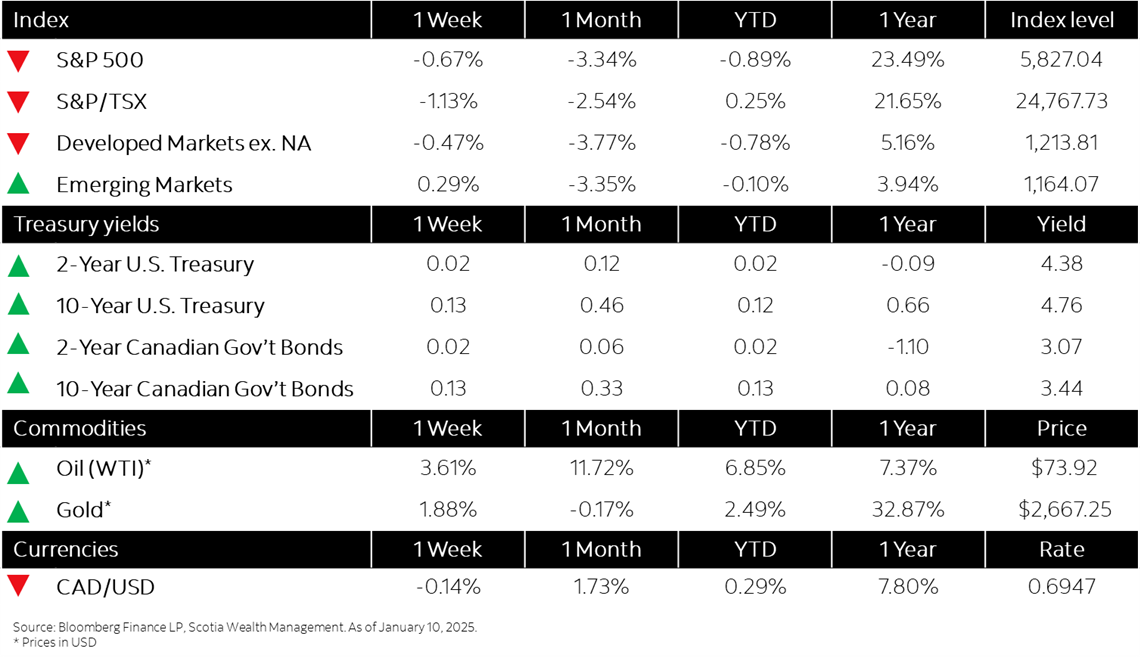

This week’s highlights

- Inflationary policy proposals, resilient labour market push equity markets lower

- Bond yields moved higher throughout the week on fears of inflationary tariffs and strong Canada, U.S. jobs reports

- Canadian exports rise in November, trade surplus with U.S. increases

- U.S. hiring blew past expectations with 256,000 jobs added in December

- Eurozone inflation rose to 2.4% in December