SPONSORED

Market Watch: December 6, 2024

Dec 9, 2024 | 10:51 AM

-

Share on Facebook

-

Share on Bluesky

-

Share on X

- Copy Link

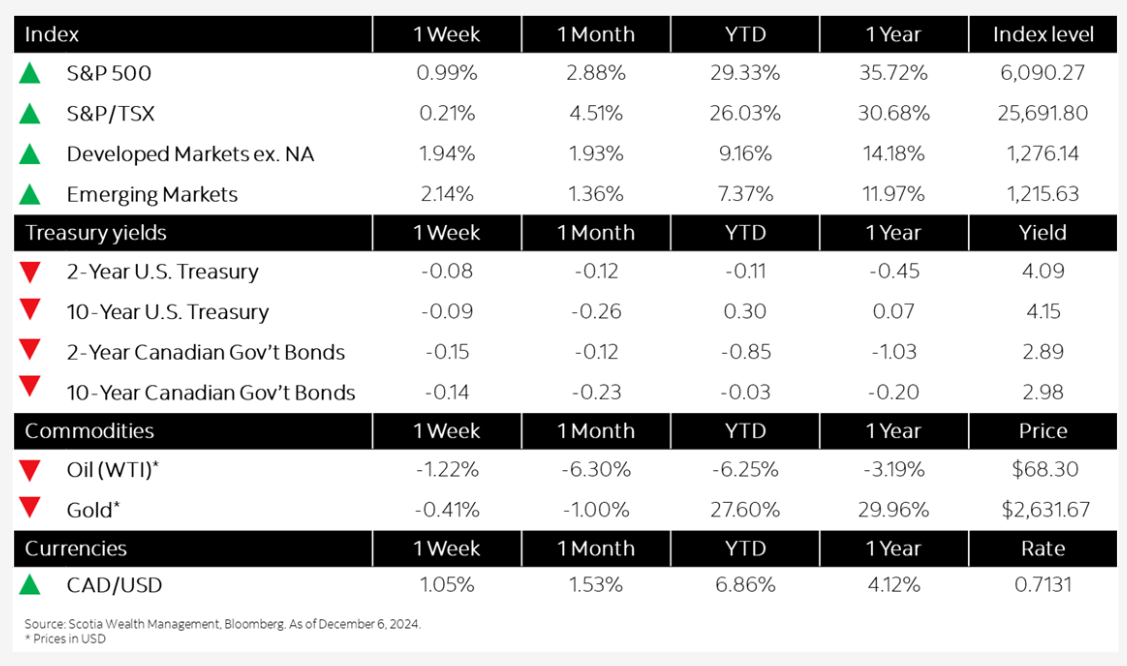

This week’s highlights

- Global markets face uncertainty amid mixed economic signals and political instability

- Indecisive Fed, jobs reports drive volatility in fixed income markets

- Canadian manufacturing activity rose at fastest pace in 21 months in November

- U.S. services sector slows as firms gauge trump policies

- China’s central bank pledges supportive policies for economy

Week in review

Global markets face uncertainty amid mixed economic signals and political instability